Texas Instruments (TXN) reported its Q1 2026 financial results on April 22, 2026, beating market expectations for both revenue and earnings per share, driven by a recovery in the industrial and data center markets.

Here is the summary of the latest earnings report:

Core Financial Performance

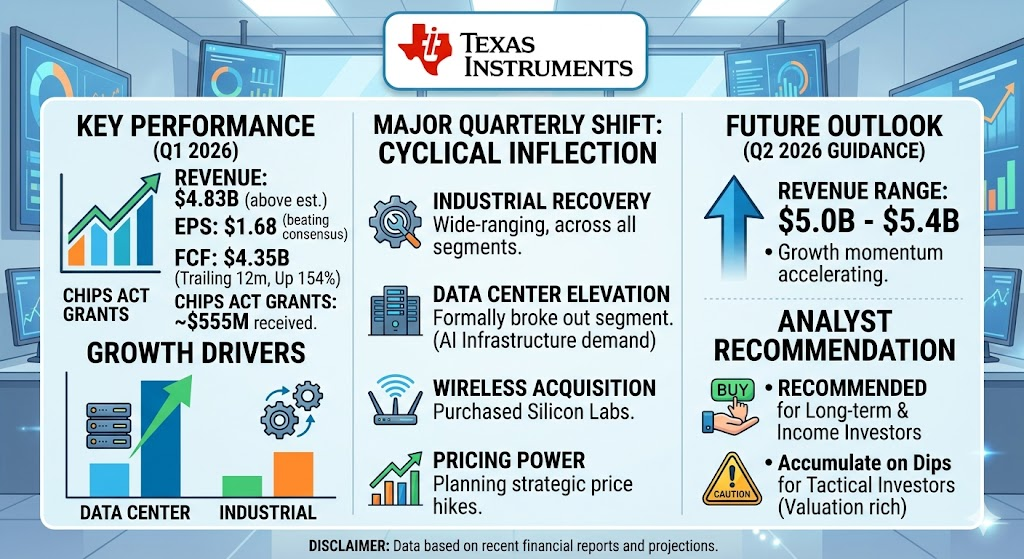

- Revenue: $4.83B, ahead of market expectations.

- Earnings Per Share (EPS): $1.68, surpassing analyst consensus.

- Cash Flow: Operating cash flow for the trailing 12 months was $7.82B, with free cash flow (FCF) reaching $4.35B, representing a 154% year-over-year increase. The company also received approximately $555M in direct grants from the US CHIPS Act during the quarter.

Business Highlights and Market Demand

- Dual Growth Engines: Growth this quarter was primarily propelled by the industrial and data center segments. Industrial customers, who had been undergoing inventory adjustments, showed signs of recovery, while data center demand driven by AI infrastructure remained robust.

- Capacity Progress: The new fabrication plant in Sherman, Texas, successfully achieved a high-volume manufacturing milestone, boosting long-term chip production capacity.

Future Outlook (Q2 2026)

- Revenue Guidance: Expected to be between $5.0B and $5.4B, indicating that growth momentum is accelerating rather than being a temporary rebound.

As the leader in analog chips, Texas Instruments’ performance is widely regarded as a bellwether for the semiconductor industry and broader economic demand. The optimistic signals from this earnings call are generally interpreted by the market as a sign that inventory depletion in industrial and automotive end markets is nearing completion and demand is turning a corner.

Texas Instruments demonstrated a significant cyclical inflection in Q1 2026, with revenue increasing 19% year-over-year and 9% sequentially, marking its fastest growth rate since the pandemic.

Here are the four core shifts and key changes highlighted in this quarter’s earnings report:

1. Breadth of Recovery Across End Markets

While previous quarters were clouded by concerns over prolonged inventory corrections in industrial and automotive chips, this quarter’s data confirmed that the industry has bottomed out:

- Core Industrial Market: Revenue surged over 20% sequentially and jumped more than 30% year-over-year. Management emphasized that this marks the first time in recent years where growth was synchronized across “all regions, all sub-segments, and all customer sizes,” indicating a broad-based macro recovery rather than isolated ordering.

- Automotive Market: Remained relatively flat sequentially but posted single-digit year-over-year growth, showing resilient stability driven largely by strong demand in the Chinese market.

- Communications Equipment: Revenue grew over 30% sequentially and roughly 25% year-over-year.

2. Formally Breaking Out the “Data Center” Segment

To reflect its rising strategic importance amid the AI server infrastructure boom, Texas Instruments officially elevated Data Centers to a standalone point of discussion starting this year.

- The data center segment delivered explosive performance this quarter, with revenue growing over 25% sequentially and soaring approximately 90% year-over-year.

- The surging demand for high power density, precise power management, and advanced signal chain chips in AI servers is rapidly becoming a major growth engine for the company.

3. Strategic Acquisition and Product Expansion

Texas Instruments announced a major strategic move this quarter by acquiring Silicon Labs, a leader in wireless semiconductor solutions.

- This acquisition is designed to instantly bolster TI’s portfolio in embedded wireless connectivity, accelerating its roadmap in the Internet of Things (IoT) and industrial intelligent edge markets.

4. Inflection Point in CapEx and Cash Flow

TI’s multi-year, $50B investment strategy to expand 300mm wafer capacity—including the newly opened Sherman, Texas (SM1) fab—had previously put significant pressure on free cash flow (FCF).

- This quarter marked a positive turning point. As new fabs began volume production and $555M in direct grants from the US CHIPS Act hit the balance sheet alongside recovering revenues, trailing 12-month FCF more than doubled from $1.7B in the prior-year period to $4.35B.

- CFO Rafael Lizardi expressed optimism that as the peak of the capital expenditure cycle begins to taper, full-year 2026 FCF per share could reach $8.00 or higher.

5. Initiating a New Round of Strategic Price Adjustments

Capitalizing on robust end-market recovery and shifts in supply chain dynamics, TI demonstrated strong pricing power. Following a price hike in April, market reports indicate that the company plans to implement a second round of product price increases effective July 1, 2026. This move is expected to offset rising depreciation costs, protect net margins (currently hovering around 29%), and support gross margin expansion moving forward.

For the upcoming quarter (Q2 2026), Texas Instruments issued financial guidance that outpaced market consensus, forecasting revenue between $5.0B and $5.4B and EPS between $1.77 and $2.05.

Based on statements from CEO Haviv Ilan and the management team, the primary growth drivers heading into the next quarter and the second half of the year center around three core dimensions:

1. Monetization of Data Center ASSPs and Socket Expansion

Following an explosive 90% year-over-year revenue surge in the data center segment during Q1, this sector will continue to act as TI’s primary growth locomotive in Q2.

- Transition to Specialty Chips: AI servers—particularly next-generation GPU clusters—demand highly complex, high-power-density, and multi-phase power delivery systems. TI’s long-term R&D investments are now entering the harvest phase, with shipments of its custom Application-Specific Standard Products (ASSPs) tailored for AI server racks expected to scale significantly.

- Market Share Gains: Management noted that because of TI’s robust 300mm manufacturing capacity and immediate inventory availability, the company successfully filled socket vacancies when competitors faced supply constraints. This supply chain advantage will continue to convert into market share gains through Q2.

2. Broad-Based Industrial Restocking and Cyclical Upside

The industrial segment’s strong bounce-back in Q1 (surging over 20% sequentially) is showing sustained momentum into the next quarter.

- Low Inventory Tailwind: Customer inventory channels have officially bottomed out, while end-market sell-through continues to show steady improvement.

- Capacity Readily Available: Because current run-rate revenue is still roughly 15% below the historical peaks of 2022, management sees substantial runway left for expansion. TI’s healthy inventory positioning allows it to capture urgent Q2 upside orders with exceptionally short lead times.

3. Pricing Power and Gross Margin Optimization

While not a volume driver, pricing strategy is set to become a vital lever for revenue and margin growth.

- CEO Haviv Ilan noted that chip pricing remained resilient and flat through Q1 and Q2, breaking away from the typical historical seasonal price declines.

- Management explicitly stated that if Q2 demand confirms the sustainability of this macro recovery, TI will likely implement strategic price adjustments in the second half of the year. This move would directly support top-line growth and help offset the depreciation headwinds from newly online fabrication plants.

Key Risk to Monitor: The Automotive Tug-of-War

In contrast to the clear visibility in industrial and data center markets, management remains cautious regarding the automotive segment for Q2. While aggressive purchasing by Chinese EV makers supports the baseline, automotive demand across western regions remains soft. The CEO cautioned: “It is still too early to declare a universal recovery in automotive; we are watching Q2 developments very closely.”

Following Texas Instruments’ stronger-than-expected Q1 2026 results and robust forward guidance, Wall Street analysts and market consensus have significantly revised their EPS outlook upward for the next 12 months.

Overall, the next year is projected to be a period of accelerating financial recovery fueled by powerful operating leverage. Current consensus estimates place full-year 2026 EPS at approximately $7.60, with the rolling forward 12-month EPS (extending into mid-2027) expected to climb into the $7.71 to $8.78 range.

Here is a detailed financial breakdown of the three core drivers and potential gross margin pressures shaping the EPS trajectory over the next year:

1. Operating Leverage Driving Accelerated EPS Rebound

TI’s financial model demonstrates massive operating leverage. In Q1, a 19% year-over-year revenue increase translated into a 36.6% surge in operating profit to $1.81B, expanding operating margins by 490 basis points to 37.5%.

- Gross Margin Recovery: With Q2 revenue guidance ($5.0B to $5.4B) confirming sustained demand, CFO Rafael Lizardi expects the profit fall-through on incremental revenue to remain at a high rate of 75% to 85%. As capacity utilization ticks up heading into the second half of the year, gross margins are projected to climb from the current 58% back toward the 60%+ threshold, serving as the strongest catalyst for EPS growth.

2. High-Margin Data Center Mix and H2 Strategic Pricing

- Product Mix Optimization: Custom application-specific power management chips (ASSPs) engineered for AI servers command high average selling prices (ASPs) and premium gross margins. As these shipments scale into volume production through late 2026 and early 2027, they will favorably mix-shift TI’s aggregate corporate margins.

- Pricing Tailwinds: Management’s signals regarding potential strategic price hikes in the second half of the year would flow directly to the bottom line, providing a clean lift to EPS in Q4 2026 and Q1 2027.

3. Headwinds Tempering the Near-Term EPS Slope

While the trajectory is decidedly positive, the EPS expansion path over the next year faces two structural financial friction points:

- Depreciation Headwinds: The Sherman, Texas (SM1) fab is now in volume production, and subsequent 300mm facilities will continue to come online over the next year. The commencement of depreciation on these massive capital investments introduces fixed-cost burdens that will partially blunt the gross margin upside.

- Silicon Labs Acquisition Drag: The newly announced acquisition of Silicon Labs is slated to close in the first half of 2027. The CFO confirmed that TI will incur ongoing deal-related and pre-closing integration expenses over the next few quarters, acting as a minor non-operating drag on quarterly EPS.

Expected Quarterly EPS Trajectory

Market consensus models a steady, stair-step progression in quarterly profitability over the next year:

- Q1 2026 (Actual): $1.68 (Beating the consensus estimate of $1.37)

- Q2 2026 (Guidance): $1.77 to $2.05 (Midpoint of $1.91, significantly above prior consensus of $1.55)

- H2 2026 to H1 2027: Driven by the dual engines of industrial restocking and data center demand, quarterly EPS is expected to stabilize above the $2.00 mark and trend toward the $2.20 to $2.25 range.

From a professional investment perspective, Texas Instruments (TXN) is currently at a highly compelling cyclical inflection point. The Q1 2026 earnings report confirmed that the industry-wide inventory drawdown has bottomed out, and the company is entering a powerful recovery phase.

However, whether to buy the stock right now depends entirely on your investment horizon and valuation discipline. Below is a structured investment thesis outlining why the stock is attractive, the near-term valuation risks, and an actionable strategy.

The Structural Buy Case (Investment Thesis)

- Explosive Operating Leverage: TI features a classic asset-heavy, high-operating-leverage financial model. With Q2 revenue guidance signaling a sustained macro recovery, incremental revenue will convert to profit at a high fall-through rate of 75% to 85%. As utilization ticks up, corporate gross margins are poised to cross back over 60%, driving an aggressive acceleration in EPS.

- The New AI Secular Growth Engine: By isolating “Data Centers” as a standalone segment, TI is showing where the high-margin growth is. AI server clusters require highly complex, multi-phase power delivery systems. The volume ramping of TI’s custom Application-Specific Standard Products (ASSPs) in H2 2026 protects the company from general analog commoditization and lifts overall average selling prices (ASPs).

- Capitalizing on a Massive Competitive Moat: TI’s controversial $50B capital expenditure campaign to build out internal 300mm wafer capacity (including the recently online Sherman, Texas fab) is transforming from a cash drag into an impenetrable moat. As industry demand returns, TI can fulfill urgent upside orders with ultra-short lead times, allowing it to systematically capture socket market share from capacity-constrained peers.

- Favorable Cash Flow Inflection: With massive capital expenditures beginning to peak and $555M in US CHIPS Act grants hitting the balance sheet, trailing 12-month free cash flow surged to $4.35B. Full-year 2026 FCF per share is on track to challenge $8.00, providing rock-solid fundamental backing for its premium dividend growth track record.

The Near-Term Valuation Risk (The Counter-Argument)

- Extremely Rich Valuation: Following the post-earnings rally, TXN has surged past $300 per share, pushing its trailing P/E ratio over 50x and its forward P/E well past 35x. This places its current valuation regime at a 10-year historic high, significantly higher than its 5-year historical average of roughly 26.7x.

- Priced for Perfection: At these levels, the market has already priced in the vast majority of the 2026–2027 industrial rebound. The average 1-year analyst price target sits near $282, indicating the stock is technically trading at a short-term premium and leaving very little margin of safety for any macroeconomic hiccups.

- Depreciation Tsunami: As the Sherman fab and other new 300mm facilities transition to volume production, heavy fixed-cost depreciation will hit the income statement. While rising revenues will dilute this impact, it will structurally cap how fast net profit margins can expand over the next 12 months.

Institutional Investment Recommendation

- For Long-Term Income & Value Investors: Buy and HoldIf your mandate focuses on wide-moat, quality businesses with unstoppable supply chain advantages and elite dividend compounding, TXN remains a core holding. Its structural cost advantage in 300mm manufacturing ensures it will dominate the analog landscape for the next decade.

- For Tactical Allocators & Growth-Oriented Portfolios: Accumulate on DipsDo not chase the stock at its current all-time highs. The current risk-reward profile is skewed to the downside for short-term capital appreciation due to overextended technicals and multiple expansion.

The ideal execution strategy is to establish a starter position via dollar-cost averaging or wait for technical consolidation. Look to build a heavier concentrated position upon a market-driven pullback toward its key moving averages or a valuation regression closer to 30x forward earnings, allowing you to capture the long-term cash flow benefits of the AI power boom with a safer entry point.

Source:

- https://investor.ti.com/news-releases/news-release-details/ti-reports-first-quarter-2026-financial-results-and-shareholder

- https://investor.ti.com/events/event-details/q1-2026-earnings-conference-call

- https://quartr.com/companies/texas-instruments-incorporated_3491

- https://www.stocktitan.net/news/TXN/ti-reports-first-quarter-2026-financial-results-and-shareholder-hzdn1u24306d.html

Back to Texas Instruments page