KLA Corporation (KLAC) released its fiscal 2026 third quarter financial results (corresponding to Q1 calendar year 2026, ended March 31, 2026) on April 29, 2026. The results exceeded the company’s previous guidance across key revenue and profitability metrics.

Here is the summary of the latest quarterly earnings:

Key Financial Metrics

Revenue: Reached 3.42B, up 11% year-over-year and 4% sequentially, beating analyst expectations of 3.36B and the midpoint of the company’s own guidance.

Gross Margin: Non-GAAP gross margin came in at 62.2%, surpassing the midpoint of guidance due to a favorable product mix.

Operating Margin: Recorded at 42.6%.

Net Income: GAAP net income was 1.20B; Non-GAAP net income reached 1.24B.

Earnings Per Share (EPS): GAAP diluted EPS was 9.12; Non-GAAP diluted EPS was 9.40, beating the market consensus of 9.17.

Cash Flow and Capital Returns: Quarterly operating cash flow was 707.5M, with free cash flow (FCF) at 622.3M. The company returned a total of 874.8M to shareholders during the quarter through dividends and share repurchases.

Business Highlights and Market Drivers

Advanced Packaging and HBM: CEO Rick Wallace highlighted that AI infrastructure buildouts continue to drive demand across foundry/logic, memory, and advanced packaging. KLA continues to extend its leadership in process control for advanced wafer-level packaging.

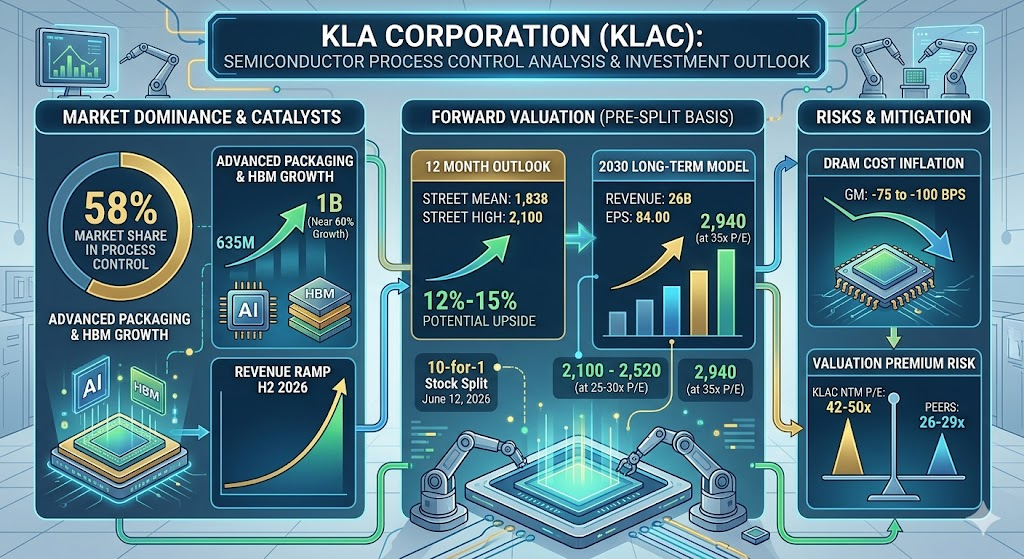

Process Control Market Share: Recent third-party industry reports indicated that KLA’s market share in the process control sector reached 58%, reinforcing its long-term growth momentum and progress toward its 2030 target model.

Capital Allocation Strategy: The Board of Directors approved an increase in the quarterly dividend to 2.30 per share (expected to be declared in May) and authorized an additional 7B for share repurchases, demonstrating confidence in long-term value creation.

Next Quarter Guidance (Fiscal Q4 2026, Ending June 2026)

Total Revenue: Projected at 3.58B, plus or minus 200M.

Non-GAAP Gross Margin: Expected to be 61.75%, plus or minus 1%.

Non-GAAP Diluted EPS: Projected at 9.87, plus or minus 1.00.

Market Reaction

Despite beating revenue and EPS expectations, the stock experienced a modest short-term correction (dipping around 3.2%) following the announcement. Market analysts attributed this to material delivery timelines and inventory adjustments that drove quarterly operating expenses slightly higher than anticipated, raising brief concerns over near-term margin pressure. However, robust demand from AI infrastructure for advanced process control continues to support a solid outlook for calendar year 2026.

Key Structural Shifts and Future Trends

Substantial Upward Revision in Advanced Packaging Revenue

This is the most defining business highlight of the quarter. Management raised its calendar year 2026 process control revenue forecast for advanced wafer-level packaging from the previous estimate of 635M to approximately 1B. This adjustment represents an explosive growth of nearly 60% in 2026, primarily fueled by aggressive customer demand for High Bandwidth Memory (HBM) and advanced logic packaging solutions.

More Optimistic Outlook for Wafer Fab Equipment (WFE) Market

KLA raised its projections for the broader semiconductor equipment industry. Management noted that due to customers actively securing tool capacity, the overall 2026 WFE market growth rate will outperform expectations from a few months ago, lifting the market forecast to a range of 120B to 130B. More importantly, management stated for the first time that visibility into calendar year 2027 is exceptional, expecting the pace of industry growth in 2027 to accelerate further relative to 2026.

Rising DRAM Prices Posing Near-Term Gross Margin Headwinds

Despite strong gross margin performance this quarter, a new cost pressure was highlighted: the recovery in the memory market has driven sharp increases in DRAM chip prices, which pushes up the manufacturing bill of materials for the image-processing computers built into KLA systems. This pricing headwind is expected to persist throughout calendar year 2026, creating a negative impact of roughly 75 to 100 basis points (0.75% – 1%) on full-year gross margins.

Significant Gains in Process Control Market Share

KLA expanded its market share in the advanced packaging process control segment by 14 percentage points compared to the same period last year. Across the broader process control sector, KLA has captured a 58% market share, a scale roughly 7 times larger than its closest technical competitor. This rising “process control intensity” allows KLA to outpace the average growth rate of the overall WFE market.

Service Business Serving as a Rock-Solid Foundation

The service business generated 775M in revenue this quarter, growing 16% year-over-year. Although it dipped 1% sequentially due to revenue recognition timing, management reiterated a long-term compound annual growth rate of 13% to 15%. Supported by a global installed base exceeding 57,000 tools, this 3B annual run-rate business continues to act as a resilient cushion against semiconductor cyclicality while providing reliable cash flows.

Muted Impact from China Export Regulations

Addressing recent US export control regulations targeting specific Chinese foundries like Hwahong Semiconductor, KLA management explicitly clarified that the financial impact on operations is immaterial and has been fully integrated into future guidance. Overall spending in the China market is anticipated to remain flat or show modest growth, avoiding any unexpected deterioration.

Core Growth Drivers for the Next Quarter and Second Half of 2026

KLA management explicitly outlined that revenue expansion and profitability momentum for the upcoming quarter (Fiscal Q4 2026) and the second half of calendar year 2026 will be sustained by three primary growth pillars and structural business drivers:

Robust Shipments to Foundry and Logic Customers

Foundry and Logic remains KLA’s most resilient revenue pillar. For the upcoming quarter, advanced logic and foundry customers are projected to contribute a substantial 82% of semiconductor process control system revenue. As global leading-edge foundries accelerate the buildout of next-generation advanced nodes, increasingly complex circuit architectures and tighter tolerance limits are significantly lifting “process control intensity” for high-end inspection and metrology tools, serving as the absolute anchor of short-term growth.

Revenue Realization from Advanced Packaging and HBM

With global AI accelerators and High Bandwidth Memory (HBM) capacity remaining severely supply-constrained, KLA’s previously accumulated advanced packaging backlogs are transitioning into physical delivery and formal revenue recognition. Management’s upward revision of 2026 advanced wafer-level packaging process control revenue to approximately 1B represents a near 60% year-over-year surge, vastly outperforming the broader packaging equipment industry’s growth average of roughly 30%. Customer urgency to secure yield for hybrid bonding and wafer-level inspection is accelerating revenue translation into the second half of the year.

Acceleration of New Greenfield Fab Shipments in H2

CFO Bren Higgins emphasized during the call that the revenue growth trajectory for the second half of 2026 exhibits a very steep slope, with the revenue ramp in the latter half of the year anticipated to be “well north of 15%.” This robust acceleration is heavily underpinned by entirely new greenfield fab constructions global customers are advancing, which are scheduled to convert into physical tool tool shipments starting later this year. The factor tempering KLA’s current revenue expansion is not customer demand or capital expenditure rollbacks, but rather semiconductor supply chain capacity limits, which the company is actively expanding to meet guaranteed second-half orders and exceptional visibility stretching into 2027.

KLA Forward One-Year EPS Trajectory and Earnings Forecast

Based on KLA’s latest earnings report, official management guidance, and updated Wall Street consensus, KLA’s earnings per share (EPS) over the forward 12 months is projected to chart a steep, back-half-loaded acceleration curve.

Additionally, KLA has announced a 10-for-1 stock split scheduled to take effect on June 12, 2026. To maintain direct comparability with recent financials, all figures detailed below are presented on a pre-split basis:

Near-Term Quarterly Projections: A Steep H2 Ramp

Market consensus indicates that KLA’s quarterly Non-GAAP EPS will unlock strong operating leverage in the second half of calendar year 2026, aligning with the projected revenue surge:

- Fiscal Q4 2026 (Ending June 2026): Official company guidance places EPS at a midpoint of 9.87 (within a tight range of 8.87 to 10.87).

- Calendar Q3 2026 (Ending September 2026): As new greenfield fab construction transitions into peak tool delivery phases, analyst consensus expects quarterly EPS to cross into double digits for the first time, reaching approximately 11.00.

- Calendar Q4 2026 (Ending December 2026): Serving as the absolute operational peak of the year, market expectations position quarterly EPS to surge to roughly 13.00, representing an explosive year-over-year growth rate of approximately 43%.

Annual Earnings Consensus

- Fiscal Year 2026 (Ending June 2026): Wall Street analysts currently project full-year EPS to land comfortably between 36.64 and 37.07.

- Forward 1-Year Rolling Outlook: Driven by the aggressive revenue slope in late 2026 and robust visibility extending into calendar year 2027, forward 12-month EPS is forecast to achieve a year-over-year growth rate of 19%.

Upside Catalyst Driving EPS Growth

- High-Margin Revenue Conversion: The upward revision of advanced packaging and HBM process control revenue from 635M to 1B, paired with a second-half revenue ramp projected “well north of 15%,” creates powerful operating leverage that flows straight to the bottom line.

- Aggressive Capital Returns: Alongside a 21% increase to the quarterly dividend, the Board’s authorization of a new 7B share repurchase program (equivalent to roughly 3.7% of outstanding shares) will actively shrink the share float, providing direct structural support to EPS.

Near-Term Headwinds Tempering EPS Leverage

- DRAM Cost Inflation: The sharp cyclical recovery in memory markets has spiked DRAM prices, elevating the bill of materials for the image-processing computers integrated into KLA systems. Management explicitly stated this will compress full-year calendar 2026 gross margins by 75 to 100 basis points (0.75% – 1%), slightly diluting the near-term conversion efficiency of revenue into EPS.

KLA Potential Stock Upside and Comprehensive Investment Analysis

Evaluating the investment value of KLA Corporation (KLAC) requires balancing its technical moat within the semiconductor supply chain, near-term operational catalysts, Wall Street consensus, and the company’s long-term internal financial targets.

Core Investment Thesis and Industry Competitiveness

KLA specializes in “Process Control”—the inspection and metrology of wafers and chips—a business model fundamentally distinct from traditional wafer fabrication equipment peers.

- Dominant Market Share: KLA commands a 58% market share in the global process control sector, a scale roughly 7 times larger than its closest competitor. As semiconductor nodes advance to 3nm, 2nm, and Angstrom generations, expanding circuit complexity increases customer reliance on KLA’s metrology and inspection systems (process control intensity).

- Advanced Packaging and HBM Revenue Realization: AI hardware builds are heavily dependent on High Bandwidth Memory (HBM) and advanced wafer-level packaging (such as CoWoS). Because packaging yields directly dictate chip shippability, KLA revised its calendar year 2026 advanced packaging process control revenue forecast upward from 635M to approximately 1B (nearly 60% year-over-year growth), demonstrating that AI demand has materialized into actual financial performance.

- Highly Visible Operational Acceleration: Management highlighted that driven by the construction and rollout of greenfield fabs worldwide, the revenue ramp trajectory for the second half of 2026 is projected to be “well north of 15%.” Additionally, visibility into calendar year 2027 suggests an industry growth pace that could outaccelerate 2026.

Wall Street Consensus and Near-Term Upside (12-Month Outlook)

Following KLA’s better-than-expected earnings results and the upward adjustment of its advanced packaging revenue guidance, major global brokerages adjusted their price targets for KLAC. Current market positioning indicates:

- Market Consensus Mean Target: Approximately 1,838. Because the current stock price trades close to this mean, near-term positive catalysts appear partially priced in by the market.

- Street-High Target: 2,100 (issued by major investment banks including Wells Fargo, Bank of America, and Citi).

- Near-Term Potential Upside: Measured against the street-high target of 2,100, the stock presents a potential upside of approximately 12% to 15% from current levels.

2030 Long-Term Financial Model and Extended Horizon Trajectory

KLA outlined its long-term strategic objectives during its Investor Day, providing a fundamental baseline for multi-year valuation modeling:

- 2030 Financial Blueprint: The company targets annual revenue of 26B and a Non-GAAP EPS of 84.00 by calendar year 2030.

- Mid-to-Long-Term Potential Valuation: If KLA successfully delivers on its 2030 target of 84.00 EPS, applying its historical average price-to-earnings (P/E) multiple of 25x to 30x yields an implied valuation range of 2,100 to 2,520. Under a more optimistic 35x P/E scenario, the long-term implied trajectory extends toward 2,940.

Operational Headwinds and Valuation Premium Risks

- Elevated Relative Valuation: KLA currently trades at a forward P/E (NTM P/E) ranging between 42x and 50x, with an NTM EV/EBITDA of roughly 35x. This sits above the average 26x to 29x NTM EV/EBITDA range seen among semiconductor equipment peers like Applied Materials (AMAT), Lam Research (LRCX), and ASML. This premium indicates that the equity enjoys a significant AI and structural moat premium, meaning future stock appreciation will depend entirely on earnings expansion rather than multiple expansion.

- DRAM Cost Inflation Pressures: The cyclical recovery in the memory market has driven sharp increases in DRAM prices, elevating the manufacturing bill of materials for the image-processing computers integrated into KLA systems. Management anticipates this will compress calendar year 2026 gross margins by 75 to 100 basis points (0.75% – 1%), slightly diluting the near-term efficiency of converting revenue into EPS.

Overall Market Positioning and Dynamics

In summary, KLA maintains a resilient competitive moat grounded in technical intensity and solid financial health. Its ability to convert operating profits into free cash flow remains intact, supported by a recent 21% quarterly dividend increase (to 2.30 per share) and a new 7B share repurchase authorization.

Furthermore, KLA’s previously announced 10-for-1 stock split is scheduled to take effect on June 12, 2026. While the split does not alter company fundamentals, it will reduce the per-share nominal price to the 180 range, lowering the entry barrier for retail investors and enhancing market liquidity. From an execution standpoint, because near-term valuations appear fully priced, market participants evaluating this asset often monitor potential pullbacks stemming from temporary gross margin concerns or broader market volatility to mitigate the risks of entering at a cyclical peak.

Source:

Back to KLA page