AT&T reported its first-quarter 2026 financial results on April 22, 2026. Here is a summary of the key financial and operational highlights:

Core Financial Results

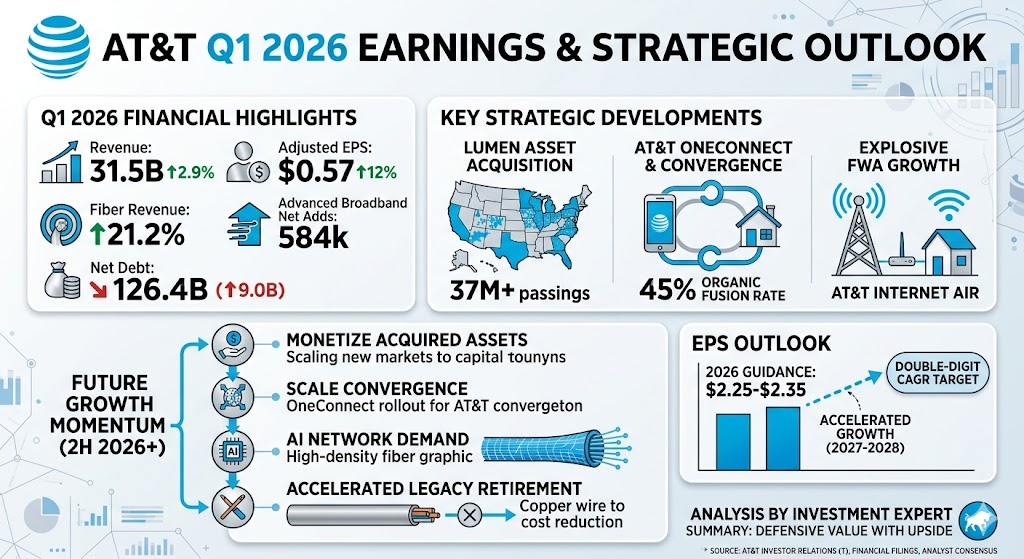

- Revenue: 31.5B, up 2.9% year-over-year, driven by growth in wireless and fiber revenues within the Advanced Connectivity segment.

- Operating Income: 6.7B, compared to 5.8B in the prior-year quarter. The operating income margin improved to 21.1% from 18.8%. Adjusted operating income was 6.9B.

- Net Income from Continuing Operations: 4.2B, down from 4.7B in the first quarter of 2025 (which included equity earnings from DIRECTV).

- Earnings Per Share (EPS): Diluted EPS was $0.54, compared to $0.61 in the prior-year quarter. Adjusted EPS was $0.57, up nearly 12% from $0.51 in the first quarter of 2025.

- Cash Flow: Operating cash flow from continuing operations was 7.6B. Free cash flow (FCF) stood at 2.5B, down from 3.1B in the year-ago period.

- Debt Profile: As of March 31, 2026, total debt was 138.4B, and net debt was 126.4B.

Segment Performance

- Advanced Connectivity:

- Segment revenue reached 28.5B, a 4.7% increase year-over-year. Fiber revenue grew 21.2%, and advanced home broadband revenue increased 27.3%.

- Retail wireless net additions were 158,000, with postpaid phone net additions at 294,000. Total retail wireless subscribers reached 109.3M at the end of the quarter.

- Fiber and fixed wireless advanced broadband net additions totaled 584,000.

- Legacy:

- Revenue was 1.8B, down 25.3% year-over-year, reflecting the ongoing secular decline of copper-based voice and data services.

- Latin America (Mexico Operations):

- Revenue reached 1.2B, an increase of 20.8% year-over-year, supported by favorable foreign exchange movements and subscriber growth.

Strategic Highlights

- The company completed the asset acquisition of Lumen’s Mass Markets Fiber Business and initiated channel and service integration.

- Capital expenditures stood at 4.9B, with total capital investment at 5.1B. Additionally, the company repurchased 2.3B of its common stock during the quarter.

Full-Year 2026 Guidance

AT&T reiterated its previously issued financial outlook for the full year:

- Service revenue growth: Low-single-digit range.

- Adjusted EBITDA growth: 3% to 4% range.

- Full-year adjusted EPS: Expected to be between $2.25 and $2.35.

- Full-year free cash flow: Expected to be 18B or higher.

During the first quarter of 2026, AT&T revealed several pivotal strategic shifts and market trends that are significantly reshaping its operational focus and financial structure:

1. Accelerated Completion of Lumen Fiber Acquisition & Post-Merger Integration

AT&T completed the asset acquisition of Lumen’s Mass Markets Fiber Business earlier than expected.

- Scale Expansion: This transaction immediately added 1.1M fiber subscribers and over 4M fiber passings, pushing AT&T’s total fiber footprint past 37M passings globally.

- Structural Shift: CFO Pascal Desroches revealed that these acquired Lumen assets will be transitioned into a Joint Venture (JV) structure. The company expects to bring in a third-party equity partner in the second half of 2026 to optimize capital efficiency.

2. Launch of “OneConnect” & Record-High Convergence Rates

The primary commercial objective this quarter focused on convergence, encouraging customers to purchase both fixed broadband and wireless mobile services.

- Platform Rollout: The company officially introduced the “AT&T OneConnect” platform, designed to offer seamless connectivity across all personal and home devices without duplicating network infrastructure.

- Metric Breakthrough: On an organic basis (excluding the Lumen acquisition), the percentage of advanced home broadband customers who also subscribe to AT&T wireless reached nearly 45%, up over 3 percentage points year-over-year. This represents the fastest annual rate of growth in company history. Currently, 42% of all advanced home broadband customers (about 5.68M accounts) are bundled with mobile services.

3. Explosive Growth in Fixed Wireless Access (FWA)

Fixed Wireless Access emerged as an equally powerful growth driver alongside traditional fiber for advanced broadband net additions.

- Out of the 584,000 total advanced broadband net additions this quarter, fiber net additions and FWA net additions (primarily driven by “AT&T Internet Air”) split the growth evenly at 292,000 each. This highlights FWA’s increasing role in capturing legacy DSL churn and expanding market share in areas where fiber builds are not yet complete.

4. Accelerated Decommissioning of Legacy Copper Networks

As the company prioritizes its 5G and fiber footprint, the retirement of legacy copper-based infrastructure has entered its most aggressive phase.

- Regulatory approval to stop offering traditional voice and data services has now been secured for 85% of legacy wire centers.

- Management intends to completely close and dismantle 30% of these approved wire centers during the second half of 2026. Reflecting this shift, legacy DSL connections declined by another 270,000 during the quarter.

5. Balance Sheet Pressure: Net Debt Spike & Lower Free Cash Flow

While Adjusted EPS and revenues showed solid growth, the immediate capital outlays for infrastructure and acquisitions triggered noticeable short-term changes to the balance sheet.

- Rising Debt: Driven primarily by the cash required to finalize the Lumen fiber asset acquisition, AT&T’s net debt increased by approximately 9.0B compared to the previous quarter.

- Cash Flow Compression: First-quarter free cash flow declined to 2.5B from 3.1B in the year-ago period. Although management reiterated that this was a function of capital expenditure timing (with total capital investment reaching 5.1B this quarter) and firmly maintained its full-year FCF guidance of 18B or higher, the near-term cash drawdown and debt expansion marked a distinct financial shift for the quarter.

According to AT&T’s first-quarter 2026 earnings call and financial reports, management indicated that future growth momentum will accelerate in the second half of 2026, beginning next quarter. The core growth engines are concentrated in the following four key areas:

1. Monetization of Acquired Lumen Assets & JV Structure Implementation

The financial and operational benefits from the Lumen Mass Markets fiber asset acquisition, which was completed ahead of schedule in Q1, will begin to materialize fully starting next quarter.

- Scaling Operations: CEO John Stankey noted that the company is currently scaling engineering, construction, and service delivery across these newly acquired metropolitan areas. This is expected to drive more robust broadband and wireless subscriber growth in the back half of the year.

- Capital Optimization: Starting next quarter, AT&T will begin transitioning these assets into a Joint Venture (JV) structure and bring in a third-party equity partner. This move will alleviate capital expenditure pressure on AT&T while injecting fresh financial momentum through asset optimization.

2. Deepening Convergence Led by “AT&T OneConnect”

The “AT&T OneConnect” platform, introduced in the first quarter, will move into a phase of full commercial rollout in the upcoming quarter.

- Driving ARPU & Retention: As this platform seamlessly integrates home broadband and mobile wireless services, management expects the convergence rate (currently near 45% on an organic basis) to climb higher. This bundling strategy is anticipated to drive Average Revenue Per User (ARPU) growth, improve Net Promoter Scores (NPS), and lower churn rates, serving as a primary top-line driver.

3. AI-Driven Demand for High-Performance Architecture

Management emphasized that the proliferation of AI applications is fundamentally transforming telecom network requirements.

- Network Architecture Advantage: Advanced AI tools require symmetrical capacity, ultra-low latency, and session control across multiple technical environments. AT&T’s sustained investment in high-density metro fiber and nationwide spectrum provides a distinct architectural advantage in capturing AI-ready connectivity demand from both enterprise and consumer markets.

4. Expansion of Advanced Connectivity Outpacing Legacy Declines

- As EBITDA for the Advanced Connectivity segment (5G and Fiber) is projected to grow by over 6% for the full year 2026, its scale is now comfortably offsetting the 20%+ structural declines seen in legacy services (Legacy VPN, copper voice, etc.). In the second half of the year, the accelerated decommissioning of copper infrastructure (with plans to close 30% of approved wire centers) will remove significant structural costs, paving the way for further margin expansion.

Based on AT&T’s latest Q1 2026 financial results, full-year guidance, and management’s medium-term outlook, the trajectory for Earnings Per Share (EPS) over the next year is characterized by solid near-term stability followed by accelerated growth in the medium term:

Full-Year 2026 Adjusted EPS Guidance

AT&T reiterated its full-year 2026 financial outlook during the recent earnings call, projecting Adjusted EPS to be between $2.25 and $2.35.

- Strong Q1 Foundation: The actual Adjusted EPS for the first quarter came in at $0.57 (beating the consensus estimate of $0.55), representing an 11.8% year-over-year increase. This provides strong backing for the full-year target.

- Market Consensus: Wall Street analysts’ current consensus estimate for full-year 2026 EPS sits at approximately $2.30, aligning perfectly with the midpoint of management’s official guidance.

Tailwinds Driving EPS Growth Over the Next Year

- Margin Expansion in Core Segments: Continued expansion in high-margin 5G wireless and fiber broadband revenue remains the primary engine. EBITDA for the Advanced Connectivity segment is projected to grow by more than 6% for the full year.

- Legacy Cost Elimination: The aggressive plan to completely close and dismantle 30% of approved legacy copper wire centers in the second half of 2026 will permanently eliminate significant structural maintenance costs, directly flowing into the bottom line.

- Share Repurchase Impact: AT&T utilized 2.3B for common stock repurchases during Q1. The reduction in total outstanding share count will provide an ongoing mathematical tailwind to EPS figures in the quarters ahead.

Potential Headwinds and Headaches

- Increased Financing Costs: Due to the cash required to finalize the Lumen fiber asset acquisition, net debt increased by approximately 9.0B last quarter, raising total net debt to 126.4B. Higher interest expenses in the short term could partially offset operational gains.

- Secular Decline of Legacy Revenue: Legacy business lines (e.g., legacy business VPNs, copper voice) continue to decline at a 20%+ annual rate. While their scale is increasingly eclipsed by Advanced Connectivity, it remains a structural headwind to manage through the end of the year.

Outlook for 2027 and Beyond

Management explicitly framed 2026 as a pivotal investment and integration year. As the newly acquired Lumen assets transition into a capital-optimized JV structure and the OneConnect platform scales up, AT&T expects Adjusted EPS growth to accelerate into the double-digit percentage range by 2027, with the momentum anticipated to sustain a double-digit CAGR through 2028.

The current consensus among Wall Street analysts leans toward a Buy or Outperform, with average target prices hovering around $30 to $31. Against the current trading price of approximately $24, this implies a potential upside of around 20% to 25%.

Evaluating a potential position in AT&T involves balancing several core structural drivers against inherent industry risks.

The Bull Case: Why You Should Buy

- Core Portfolio Improvement: High-margin 5G mobile and fiber revenues are scaling efficiently. Advanced Connectivity EBITDA is projected to grow by over 6% for the full year, comfortably offsetting the 20%+ decline in legacy copper operations. The planned decommissioning of 30% of approved legacy wire centers in the second half of the year will permanently remove severe maintenance costs.

- Deepening Competitive Moat via Convergence: The rollout of the OneConnect platform is pushing bundling rates to a historic high of 45% on an organic basis. In the telecom sector, cross-selling broadband and wireless services increases Average Revenue Per User (ARPU) and dramatically lowers customer churn, reducing high subscriber acquisition expenses.

- Flexible Asset Optimization: Closing the Lumen fiber asset acquisition ahead of schedule expands AT&T’s network footprint past 37 million locations. Shifting these newly acquired assets into a Joint Venture (JV) structure with third-party equity partners in the back half of the year allows AT&T to capitalize on the footprint without completely overwhelming its own capital expenditure lines.

- Reliable Dividend Cushion and Buybacks: Yielding a reliable 4.5% to 4.6%, the dividend remains well-protected with a payout ratio sitting comfortably around 35% to 40% of earnings and cash flow. Supported by an ongoing share repurchase program ($2.3B spent in Q1 alone), the equity benefits from a substantial valuation floor.

The Bear Case: Reasons for Caution

- Elevated Debt and Interest Expense: Finalizing the Lumen asset purchase caused net debt to increase by roughly 9.0B last quarter, raising the total net debt load to 126.4B. In a sustained higher-rate environment, the accompanying interest expenses draw on near-term cash flow, as seen in the drop in Q1 free cash flow to 2.5B. This leverage acts as a structural ceiling on Price-to-Earnings (P/E) multiple expansion.

- Low Organic Growth Ceiling: Telecom remains a highly saturated, capital-intensive utility market. Even if management successfully hits its targeted double-digit EPS compound annual growth rate (CAGR) for 2027–2028, that growth will stem almost entirely from aggressive cost-cutting and market-share consolidation rather than secular expansion of the broader addressable market.

Final Investment Recommendation

An investment in AT&T depends primarily on portfolio objectives and risk tolerance:

- Suitable for Income and Value Investors: For portfolios targeting steady cash flows, robust defensive posture, or secure high-dividend exposure, AT&T represents an excellent opportunity. The underlying business turnaround is stable, making the stock a reliable safe haven during broader market volatility.

- Unsuitable for Growth Seekers: For portfolios requiring aggressive top-line acceleration, major capital appreciation, or high-beta technological upside, AT&T should be avoided. The company offers predictable operational optimization rather than explosive disruption.

Source:

- https://about.att.com/story/2026/1q-earnings.html

- https://investors.att.com/~/media/Files/A/ATT-IR-V2/financial-reports/quarterly-earnings/2026/1Q-2026/1Q26_ATT_Earnings_Slides.pdf

- https://www.investing.com/news/sec-filings/att-reports-firstquarter-earnings-of-42-billion-revenue-rises-29-93CH-4628573

- https://www.telecomtv.com/content/access-evolution/at-t-reports-strong-first-quarter-2026-financial-results-55346/

- https://www.stocktitan.net/sec-filings/T/8-k-at-t-inc-reports-material-event-9a06c6264434.html

Bck to AT&T page