Founding and the Bell System Monopoly (1877–1983)

Establishment of the Bell Telephone Company (1877)

Alexander Graham Bell, the inventor of the telephone, founded the Bell Telephone Company. In 1885, its subsidiary, the American Telephone and Telegraph Company (AT&T), was incorporated to build and operate the long-distance telephone network. In 1899, AT&T under went a corporate restructuring, acquiring the assets of its parent company and officially becoming the headquarters of the entire Bell System.

The “Ma Bell” Monopoly (Early 20th Century–1980s)

Under a government-sanctioned “natural monopoly” framework, AT&T built a massive empire known as the Bell System (commonly called Ma Bell). It consisted of regional Bell companies handling local service, AT&T Long Lines managing long-distance networks, and Western Electric manufacturing telecommunications equipment, altogether controlling nearly 80% of the US telecommunications market. During this era, its R&D arm, Bell Labs, invented groundbreaking technologies including the transistor, lasers, and the Unix operating system.

Divestiture and the Rise of SBC (1984–2004)

The Antitrust Settlement and Breakup (1984)

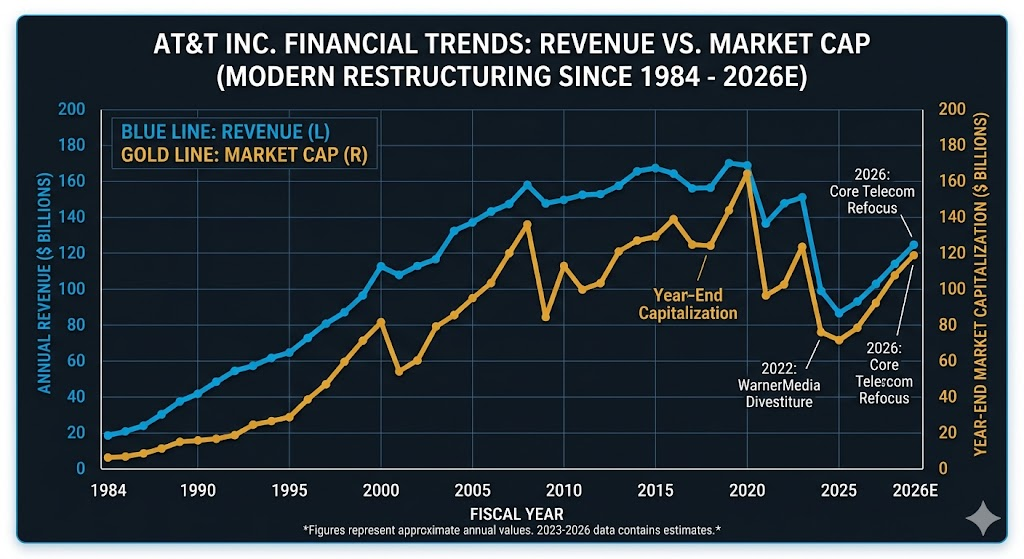

Following a protracted antitrust lawsuit filed by the US Department of Justice, AT&T agreed to a consent decree that led to its breakup in 1984. The corporation retained its long-distance business and Bell Labs, while its local telephone operations were split into seven independent Regional Bell Operating Companies, affectionately known as the “Baby Bells.”

Expansion of Southwestern Bell

Among the Baby Bells, Southwestern Bell Corporation (SBC) pursued the most aggressive growth strategy. As deregulation reshaped the telecom sector, SBC executed a series of major acquisitions, purchasing Pacific Telesis and Ameritech to become a dominant multi-regional carrier.

Rebranding and Reclaiming the Throne (2005–2014)

SBC Acquires Its Former Parent (2005)

The original AT&T, stripped of its local exchange networks, struggled to compete in the changing market. In 2005, SBC acquired its former parent company for 16 billion dollars. Upon completion of the merger, SBC retired its own corporate name and adopted the globally recognized “AT&T” brand for the newly combined entity.

The 4G Era and Smartphone Boom (2007 onward)

The reconstituted AT&T secured a massive competitive advantage in 2007 by becoming the exclusive US carrier for the original Apple iPhone. This partnership drove a massive surge in mobile data subscribers. The company subsequently directed capital into building its 4G LTE network, establishing a fierce duopoly at the top of the US wireless market alongside Verizon.

Media Expansion and Strategic Refocus (2015–Present)

Building a Media Empire (2015–2018)

Seeking new growth engines beyond traditional telecom services, AT&T embarked on an aggressive diversification strategy. It acquired satellite television provider DirecTV for 48.5B dollars in 2015, followed by a hard-fought 85B dollars acquisition of Time Warner in 2018. The media giant, home to HBO, Warner Bros., and CNN, was renamed WarnerMedia, aiming to fuse premium content with distribution channels.

Debt Pressures and Returning to Core Telecom (2021 onward)

The massive acquisition spree saddled AT&T with significant debt, just as the streaming wars intensified. Recognizing the shift, leadership executed a rapid strategic pivot. AT&T spun off DirecTV in 2021 and completed the divestiture of WarnerMedia in 2022, merging it with Discovery to form Warner Bros. Discovery.

Having streamlined its corporate structure, AT&T shifted its full attention back to its core telecom roots, focusing capital expenditures on expanding 5G wireless coverage and fiber-optic broadband networks.

Industry Landscape: The Big Three Oligopoly

The US telecommunications market is highly consolidated into a mature oligopoly dominated by three infrastructure-based giants: AT&T, Verizon, and T-Mobile.

- T-Mobile (The Mobile Share Leader)Following its merger with Sprint, T-Mobile secured a massive lead in mid-band 5G spectrum assets. It currently paces the industry in wireless subscriber growth and 5G coverage velocity. Its aggressive “Un-carrier” consumer pricing continues to exert top-line pressure on AT&T’s retail mobility business.

- Verizon (The Premium Standard)Historically recognized for network reliability and premium enterprise market share, Verizon commands the highest average revenue per user (ARPU) in the industry. While its early 5G strategy suffered from over-indexing on short-range millimeter wave (mmWave) spectrum, it is aggressively deploying mid-band C-Band assets to defend its premium consumer and corporate accounts against AT&T.

- AT&T (The Ubiquitous Connectivity Provider)After unwinding its costly media diversification strategy, AT&T has refocused on a dual-engine infrastructure playbook: 5G mobility and fiber-to-the-home (FTTH). Its central commercial thesis relies on leveraging extensive fiber deployment to cross-sell premium wireless mobility packages to residential and enterprise customers.

AT&T’s Competitive Advantages

- Fiber and 5G ConvergenceAT&T operates one of the largest fiber-optic broadband networks in the United States. Fiber infrastructure functions as a high-margin revenue contributor and serves as the essential backhaul architecture required to support dense 5G cell sites. This converged footprint allows AT&T to offer premium “fiber plus wireless” bundling, which structurally reduces customer churn rates.

- Enterprise and Government MoatAT&T maintains deeply entrenched relationships within large-scale enterprise networks, industrial IoT connectivity, and federal defense contracts. A key component of this institutional moat is FirstNet, the exclusive nationwide wireless communications platform built for first responders. This government-backed network provides high-margin, sticky revenue that competitors cannot easily displace.

- Streamlined Capital AllocationBy completing the divestitures of WarnerMedia and DirecTV, AT&T successfully removed non-core operational distractions and heavy debt overhangs. Capital expenditures (CapEx) are now strictly aligned with pure-play telecom infrastructure. The resulting stabilization in free cash flow (FCF) supports debt reduction and consistent dividend yields for value investors.

Strategic Challenges and Market Threats

- Cable MVNO EncroachmentMajor cable operators like Comcast (Xfinity Mobile) and Charter (Spectrum Mobile) are aggressively expanding via MVNO (Mobile Virtual Network Operator) agreements. By offering highly discounted wireless lines bundled with existing residential cable broadband, these players are steadily capturing cost-conscious subscriber segments from traditional wireless carriers.

- Spectrum Depletion and Cost PressuresWhile AT&T invested heavily in recent C-Band auctions, T-Mobile still maintains a broader, more continuous mid-band spectrum position. Acquiring, deploying, and optimizing future spectrum bands to keep pace with soaring data consumption remains a perpetual, multi-billion-dollar capital drain.

- Market Saturation and Price ErosionThe US smartphone market has reached absolute saturation, driving up subscriber acquisition costs (SAC) as carriers fight over the same user base. As the initial marketing lift of the 5G upgrade cycle normalizes, the sector faces a constant risk of promotional price wars, which could compress EBITDA margins if next-generation monetization models (such as standalone 5G private networks or satellite-to-cell integrations) fail to scale.

Source:

Back to AT&T page