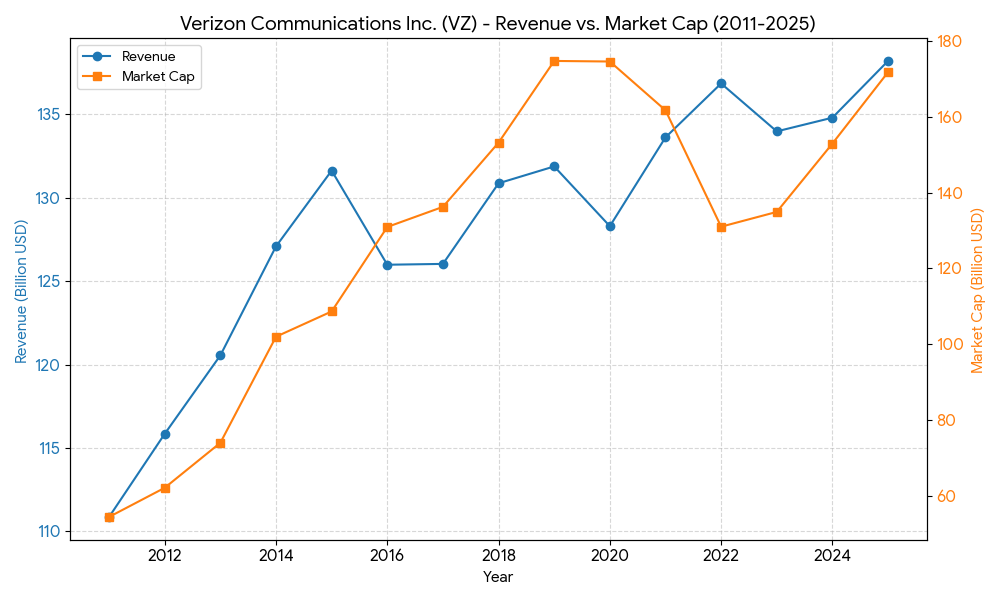

Foundation and Predecessors (1983–2000): The Merger of Regional Bell Companies

The roots of Verizon can be traced back to the 1983 breakup of the American telecom giant AT&T. Due to antitrust lawsuits, AT&T was dissolved and split into seven Regional Bell Operating Companies, commonly known as Baby Bells. One of these companies was Bell Atlantic, which primarily served the mid-Atlantic region of the United States.

In 1997, Bell Atlantic merged with NYNEX, another Baby Bell, expanding its footprint into the northeastern United States.

Birth of the Brand and Rise of Mobile (2000–2010): Becoming a Telecom Giant

The year 2000 marked a pivotal turning point in the company’s history. Bell Atlantic merged with GTE, a pioneer in US wireless telecommunications, in a transaction valued at 64.7B. Following the merger, the newly formed company was officially renamed Verizon Communications. The name is a portmanteau of the Latin word veritas (meaning truth) and horizon.

During the same period, Verizon partnered with Vodafone, a UK-based telecom company, to establish a joint venture named Verizon Wireless, with Verizon holding the controlling stake. Relying on extensive network coverage and reliable signal quality, Verizon Wireless rapidly grew into one of the largest wireless service providers in the United States.

Expansion and Full Ownership (2011–2015): The 4G Era and Absolute Control

As smartphones became ubiquitous, Verizon began large-scale deployment of its 4G LTE network in late 2010, securing a leading position in technology.

In 2014, Verizon executed one of the most iconic deals in corporate history. The company acquired the 45% stake in Verizon Wireless held by Vodafone for a staggering 130B. This acquisition gave Verizon complete ownership and control over the most profitable wireless carrier in the United States.

Digital Media and 5G Transformation (2015–2020): Media Experiments and Core Restructuring

To seek new growth engines beyond traditional telecom services, Verizon acquired AOL (America Online) for 4.4B in 2015, followed by the acquisition of Yahoo’s core internet assets for 4.48B in 2017. These two internet pioneers were integrated into a digital media division named Oath, which was later renamed Verizon Media.

Concurrently, the company poured immense resources into 5G network infrastructure. In 2019, Verizon launched the world’s first commercial 5G mobile network in select US cities, heavily prioritizing ultra-high-frequency millimeter wave (mmWave) technology.

Return to the Core and Tech Infrastructure (2021–Present): Focusing on Network and Connectivity

The venture into digital media did not yield the anticipated synergies. In 2021, Verizon decided to divest the business, selling a 90% stake in Verizon Media to Apollo Global Management, a private equity firm, for 5B, while retaining only a 10% stake.

After offloading its media assets, Verizon refocused entirely on its core telecom business. In the 2021 US C-Band spectrum auction, Verizon spent over 45B in bids to compensate for its coverage gaps in the mid-band frequency. Today, Verizon focuses on expanding its 5G Ultra Wideband network, shifting its strategic emphasis toward Fixed Wireless Access (FWA) broadband, private 5G networks for enterprises, and Internet of Things (IoT) core communication infrastructure.

The US telecommunications market has long been divided among the Big Three, forming a highly concentrated oligopoly. While Verizon remains robust in terms of total revenue and subscriber loyalty, it has faced intense market share battles in recent years.

The following is an analysis of the current competitive landscape:

Market Share Tug-of-War Among the Big Three

In terms of wireless subscribers, the market shares of the top three carriers are neck and neck, turning the competition into a fierce zero-sum game in a mature market:

- T-Mobile US: Holds a market share of approximately 34.7% (around 129.5 million subscribers). After acquiring Sprint and successfully unlocking its mid-band 5G advantage, T-Mobile has led the industry in subscriber growth rate in recent years and is currently planning to further acquire UScellular’s wireless operations to expand its scale.

- AT&T: Holds a market share of approximately 31.5% (around 117.9 million subscribers). Its recent strategy focuses heavily on “Convergence” (integrating fiber and wireless), which has successfully boosted customer stickiness and lowered churn rates.

- Verizon: Holds a market share of approximately 30.8% (around 115 million subscribers). Although its wireless subscriber count slightly trails the other two, Verizon possesses the largest overall customer base in the US (including enterprise clients, totaling roughly 147 million users) and continues to maintain an industry-leading position in Average Revenue Per User (ARPU) and overall network quality evaluations.

Recent Competitive Focuses

1. The Broadband and Fiber War

Since the traditional mobile subscription market has reached saturation, fixed broadband and fiber optic networks have become the new battleground. To counter AT&T and cable operators (such as Comcast and Charter), Verizon announced an all-cash acquisition of Frontier Communications for 20B in late 2024. This move significantly expands its fiber footprint and strengthens its competitiveness in the broadband market.

2. The Proliferation of Fixed Wireless Access (FWA)

Verizon is actively leveraging its 5G network to roll out home and business wireless broadband services (Fixed Wireless Access), directly challenging traditional cable broadband providers. This business segment has currently become Verizon’s primary engine for new revenue growth.

3. Catching Up in C-Band Deployment

In the early stages, Verizon over-indexed on millimeter wave (mmWave) technology, causing its mid-band 5G coverage to temporarily fall behind T-Mobile, which possessed abundant mid-band spectrum. Subsequently, Verizon spent over 45B in the C-Band auction and has aggressively accelerated cell site deployment in recent years. Earnings reports from early 2026 show that its postpaid phone net additions hit a five-year high, indicating that the spectrum reinforcement has successfully recaptured subscriber growth momentum.

Coopetition: The Newly Formed Joint Venture

Despite the intense market competition, facing the persistent wireless dead zones across the US (particularly in remote areas), the Big Three (Verizon, AT&T, and T-Mobile) reached an agreement in principle in May 2026 to form a brand-new joint venture. By pooling their constrained spectrum resources to expand overall network capacity, they aim to collectively enhance customer experience in rural areas and unify their interfacing with satellite communication providers. This demonstrates that when confronted with massive infrastructure costs, the telecom industry is shifting from absolute competition toward strategic cooperation.

Source:

Back to Verizon page