Bank of America (BAC) reported its first quarter 2026 financial results on April 15, 2026, delivering performance that exceeded analyst expectations. Below is a summary of the quarterly report:

Key Financial Data

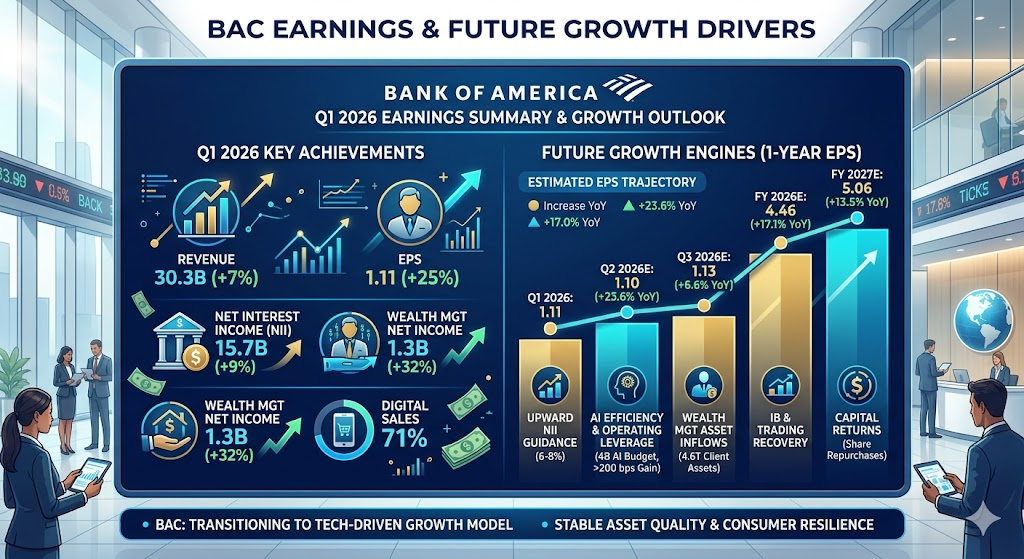

- Revenue: 30.3B, up 7% year-over-year (surpassing the expected 29.9B).

- Net Income: 8.6B, an increase of approximately 17% from 7.4B in the previous year.

- Earnings Per Share (EPS): 1.11, up 25% from 0.89 in the previous year (beating the expected 1.01).

- Net Interest Income (NII): 15.7B, up 9% year-over-year, primarily driven by growth in loan and deposit balances and the repricing of fixed-rate assets.

Business Segment Performance

- Wealth and Investment Management: Performance was particularly strong, with net income reaching 1.3B (up 32% year-over-year) and record revenue of 6.7B, mainly due to higher asset management fees driven by market valuation gains.

- Consumer Banking: Digital progress continued, with digital channel sales accounting for 71% of total sales.

- Investment Banking and Trading: Both investment banking fees and sales/trading revenue achieved double-digit growth.

Asset Quality and Efficiency

- Efficiency Ratio: Optimized to 61.22% (compared to 62.91% in the same period last year).

- Provision for Credit Losses: Decreased to 1.3B (from 1.5B last year), reflecting relatively stable asset quality.

- CET1 Capital Ratio: 11.2%, exceeding the regulatory threshold of 10%.

Shareholder Returns

- Share Repurchases: The company repurchased 7.2B worth of common stock during the quarter.

- Dividends: Paid 2.0B in common stock dividends, maintaining a quarterly payout of 0.28 per share.

In the Q1 2026 earnings report, Bank of America (BAC) demonstrated several key strategic and financial shifts, indicating the company is transitioning from the high-interest-rate environment of the past two years toward a more comprehensive, technology-driven growth model.

1. Upward Revision of Net Interest Income (NII) Outlook

Management raised the full-year 2026 NII growth guidance to 6%-8%. This change occurred as interest rate expectations shifted from “multiple rate cuts” to “higher for longer,” allowing the bank to benefit from elevated loan rates for an extended period. Additionally, the repricing of fixed-rate assets continues to drive revenue momentum.

2. Efficiency Dividends from AI Implementation

The quarterly report significantly highlighted the concrete contributions of Artificial Intelligence (AI) to business operations, moving beyond mere concepts.

- Meeting Journey AI: This new tool has begun helping financial advisors improve productivity and is cited as a factor in the profit growth of the wealth management business.

- Operational Efficiency: Through AI and automated processes, the bank successfully optimized its efficiency ratio to 61%, achieving “Operating Leverage” where revenue growth outpaces expense growth.

3. Diversification of Business Structure

Beyond traditional deposit and loan activities, growth this quarter relied heavily on non-interest income:

- Equity Trading and IB Fees: Equity trading revenue hit record highs, and investment banking fees rose 21% year-over-year, indicating a significant recovery in Mergers and Acquisitions (M&A) and equity financing activities.

- Wealth Management Scale: Client assets reached a new peak of 4.6 trillion, with growth in asset management fees becoming a cornerstone of stable profitability.

4. Accelerated Digital Channel Transformation

Within consumer banking, digital sales as a percentage of total sales climbed to 71% from 65% last year. This not only reduces the operating costs of physical branches but also makes the bank more competitive in acquiring new customers (netting over 100,000 new accounts this quarter).

5. Resilience in Asset Quality

Despite ongoing macroeconomic uncertainty, the provision for credit losses unexpectedly decreased this quarter. Net charge-offs remained within a controllable range, suggesting that the credit health of the customer base is performing better than the market’s previous pessimistic expectations.

According to the Q1 2026 earnings call and the latest management guidance, Bank of America’s (BAC) growth momentum for the next quarter and throughout 2026 will focus on the following five core engines:

1. Upward Revision of Net Interest Income (NII) Guidance

As market expectations for Federal Reserve rate cuts shifted from “multiple cuts” to “higher for longer,” Bank of America raised its full-year 2026 NII growth target from 5%-7% to 6%-8%. This indicates that in the coming quarter, the bank will continue to benefit from elevated loan spreads and the yield gains from repricing fixed-rate assets upon maturity.

2. AI-Driven Operating Leverage

Bank of America has allocated a technology budget of 13B for 2026, with 4B specifically dedicated to Generative AI and machine learning.

- Efficiency Gains: Erica, the AI assistant, has surpassed 3.2 billion interactions, handling 98% of basic customer inquiries and significantly reducing labor costs.

- Operating Leverage: Management reaffirmed its goal to achieve over 200 basis points of “Positive Operating Leverage” in 2026 (meaning revenue growth outpaces expense growth by more than 2%), which will directly translate into net income growth next quarter.

3. Asset Inflows in Wealth Management

The wealth management segments (Merrill and Private Bank) are showing strong momentum:

- Asset Scale: Client balances have reached 4.6 trillion. With asset valuation increases driven by a recovering stock market, “Asset Management Fees” are expected to maintain double-digit growth next quarter.

- Client Activity: The continuous inflow of new clients and the digitalization of advisory services (such as Meeting Journey AI) will keep profitability at high levels.

4. Recovery in Investment Banking and Trading

With the rebound in Mergers and Acquisitions (M&A) activity and equity financing demand, Bank of America expects investment banking advisory fees to remain strong in the next quarter. Simultaneously, Sales & Trading revenue retains growth potential due to hedging demands sparked by macroeconomic volatility.

5. Capital Returns and Regulatory Tailwinds

- Share Repurchases: Following the relaxation of certain capital requirements by regulators, Bank of America expects to accelerate share repurchases in the second half of 2026 (following the end of Q2).

- Consumer Resilience: Continued growth in new account openings in consumer banking (netting 100,000 accounts this quarter) has driven higher transaction volumes for Zelle and digital payment systems, providing a steady stream of fee income.

Based on consensus forecasts from market analysts and the latest guidance from Bank of America (BAC) management, the Earnings Per Share (EPS) for the coming year (2026–2027) is expected to follow a steady upward growth curve.

EPS Forecast Outlook

According to recent consensus estimates from Zacks and Wall Street analysts, the EPS for Q2 2026 (expected to be released on July 14) is projected at 1.10, representing a 23.6% increase year-over-year. For Q3 2026, the EPS is expected to grow further to 1.13.

From an annual perspective, the full-year 2026 EPS estimate has been revised upward to 4.46, a 17.1% increase. Moving into 2027, growth momentum is expected to persist, with a full-year EPS target of 5.06, up approximately 13.5%.

Core Growth Drivers

1. Upward Revision of NII Guidance

As the Federal Reserve maintains interest rates at higher levels for longer than initially anticipated, BAC has raised its full-year 2026 Net Interest Income (NII) growth target to 6%–8%. This provides a solid profit foundation for the next four quarters, as the bank continues to benefit from wider loan spreads and the repricing of fixed-rate assets.

2. Operating Leverage and AI Efficiency

Bank of America is demonstrating strong “positive operating leverage,” with revenue growth expected to outpace expense growth by more than 200 basis points in 2026. By investing 4B annually in generative AI and automation, the bank is scaling its operations without significantly increasing headcount, allowing revenue gains to flow more efficiently to the bottom-line EPS.

3. Multiplier Effect of Share Repurchases

Supported by a strong 11.2% CET1 Ratio, Bank of America has the capacity to accelerate share repurchases in the second half of 2026. As the total number of outstanding shares decreases, the EPS will receive a passive boost due to a smaller denominator, even if net income remains stable.

4. Optimized Fee Income Structure

With the recovery of investment banking (M&A and financing) and wealth management assets reaching 4.6 trillion, the bank is generating steady management fee income. BAC’s shift toward “asset-light, high-margin” business lines improves the overall quality of earnings and supports long-term EPS expansion.

Potential Risk Factors

While the EPS outlook is optimistic, credit quality remains a key metric to watch. If an unexpected rise in unemployment late in 2026 leads to higher provisions for credit losses, it could erode short-term EPS. Additionally, if the macroeconomic environment triggers faster-than-expected rate cuts, the growth space for NII may be compressed.

Source:

- https://www.stocktitan.net/sec-filings/BAC/10-q-bank-of-america-corp-de-quarterly-earnings-report-bbde598aeccb.html

- https://www.investing.com/news/transcripts/earnings-call-transcript-bank-of-america-beats-q1-2026-earnings-estimates-93CH-4616137

- https://www.familywealthreport.com/article.php/Bank-Of-America-Wealth%2C-Investment-Management-Profits%2C-Revenue-Up-Q1-2026

- https://www.alpha-sense.com/earnings/bac/

- https://www.marketbeat.com/instant-alerts/bank-of-america-q1-earnings-call-highlights-2026-04-15/

- https://simplywall.st/stocks/us/banks/nyse-bac/bank-of-america/news/bank-of-americas-standout-quarter-blends-record-trading-and

- https://seekingalpha.com/news/4575382-bank-of-america-raises-2026-nii-growth-outlook-to-6-percentminus-8-percent-as-it-targets-200

- https://markets.financialcontent.com/stocks/article/finterra-2026-3-24-bank-of-america-bac-the-2026-deep-dive-on-consumer-resilience-and-the-ai-banking-revolution

- https://www.zacks.com/stock/quote/BAC/detailed-earning-estimates

- https://www.chartmill.com/stock/quote/BAC/analyst-ratings

Back to Bank of America page