Johnson & Johnson (JNJ) released its Q1 2026 financial results on April 14, 2026. Despite facing patent expirations and market competition, the company demonstrated strong revenue growth and raised its full-year guidance.

The following is a summary of the earnings analysis:

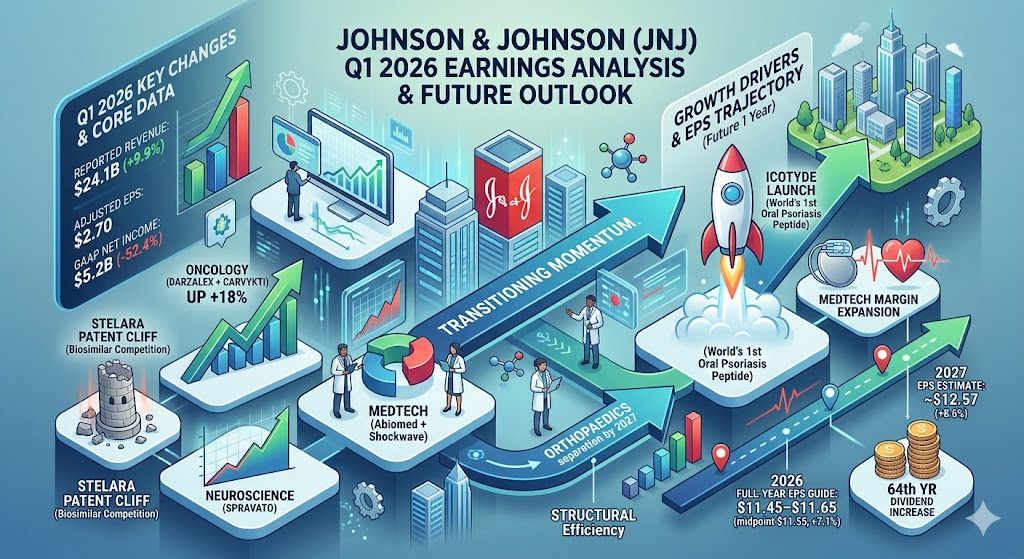

Core Financial Data

Reported revenue for the quarter was 24.1B, representing a 9.9% increase year-over-year (YoY), exceeding analyst expectations. Adjusted EPS stood at $2.70, a slight decrease of 2.5% YoY but still higher than the market estimate of $2.67. Due to acquisition costs and a high base from the previous year, GAAP net income was 5.2B, down 52.4%. Free cash flow was approximately 1.5B, compared to 3.4B in the same period last year.

Business Segment Performance

- Innovative Medicine: Revenue reached 15.43B, an 11.2% increase. Growth was primarily driven by oncology drugs (such as DARZALEX and CARVYKTI) and neuroscience treatments (SPRAVATO). While the blockbuster drug STELARA faces pressure from biosimilars, the overall impact remains manageable for now.

- MedTech: Revenue reached 8.64B, up 7.7%. The cardiovascular business performed exceptionally well with 13% growth, largely due to the integration effects of acquiring Abiomed and Shockwave, alongside rising demand for electrophysiology products. However, Volume-Based Procurement (VBP) policies in China have exerted pressure on profit margins in this segment.

Future Outlook and Guidance

- Upward Revision of Full-Year Guidance: The company raised its 2026 full-year revenue guidance to a range of 100.3B to 101.3B (midpoint of 100.8B), reflecting an estimated growth of 7.0%. The adjusted EPS guidance was also raised to $11.45–$11.65.

- Dividend Policy: A 3.1% increase in the quarterly dividend was announced, rising from $1.30 to $1.34, marking the company’s 64th consecutive year of dividend increases.

- Pipeline Momentum: Several major approvals were secured this quarter, including the oral peptide ICOTYDE for psoriasis and the VARIPULSE pulsed field ablation system in Europe.

Market Analysis and Risks

- Patent Cliff: Investors remain focused on the erosion rate of STELARA as more biosimilars enter the market throughout 2026, as this will determine if the company can maintain its long-term double-digit growth targets.

- M&A Integration: Recent acquisitions of assets like Shockwave have boosted revenue but have also diluted net profit margins and cash flow in the short term.

- Geopolitical Policy: Policy-driven price reductions in the Chinese market remain a primary headwind for the MedTech division, with the impact expected to be more pronounced in the second half of the year.

The Johnson & Johnson Q1 2026 earnings report highlights a strategic pivot where new drug approvals and surgical technology acquisitions are successfully offsetting the anticipated “patent cliff” of legacy products. Here are the most significant changes this quarter:

1. Innovative Medicine: Pipeline Success Balancing Patent Erosion

- STELARA Resistance: While STELARA faced significant biosimilar competition—creating a 920 basis point headwind—total segment revenue still grew by 11.2%. This was driven by the exceptional performance of DARZALEX (up 18%) and the rapid scaling of CARVYKTI and SPRAVATO.

- Breakthrough Approvals: The quarter saw the landmark FDA approval of ICOTYDE, the first oral peptide for psoriasis. Additionally, the expanded approval of TECVAYLI for second-line multiple myeloma treatment provides a critical long-term growth engine.

2. MedTech: Cardiovascular Expansion via M&A

- Inorganic Growth: The MedTech segment grew 7.7%, led by a 13% surge in cardiovascular revenue. This shift is a direct result of the integration of Abiomed and Shockwave Medical, positioning J&J as a leader in heart recovery and intravascular lithotripsy.

- PFA Technology: The European approval of the VARIPULSE pulsed field ablation system marks a shift in how the company competes in the atrial fibrillation market, moving toward more precise, non-thermal ablation technologies.

3. Geopolitical and Structural Shifts

- China VBP Impact: Volume-Based Procurement (VBP) policies in China continue to squeeze margins, particularly in the surgery sub-segment. Management indicated that these policy headwinds are expected to intensify in the second half of 2026.

- Orthopaedics Restructuring: The company progressed with its plan to separate the Orthopaedics business into a more autonomous unit, allowing the broader MedTech division to focus on higher-growth, higher-margin surgical and cardiovascular assets.

4. Financial Health and Shareholder Returns

- Profitability Volatility: GAAP net income fell 52.4% to 5.2B. This decline is largely attributed to the heavy costs associated with recent acquisitions and a high comparative base from the prior year. Free cash flow also dipped to 1.5B due to these integration expenses and debt repayments.

- Dividend Milestone: J&J increased its quarterly dividend by 3.1% to $1.34 per share. This marks the 64th consecutive year of dividend increases, reinforcing its status as a “Dividend King” despite the current phase of high capital expenditure.

Looking toward the second quarter and the remainder of 2026, Johnson & Johnson’s growth momentum is transitioning from M&A integration toward the commercialization of breakthrough therapies and the penetration of high-margin medical technologies.

The following are the core growth engines for the next quarter:

1. Innovative Medicine: Blockbuster Launches and Label Expansions

- ICOTYDE Market Launch: As the world’s first oral peptide therapy for psoriasis (targeting IL-23), ICOTYDE is expected to be one of the largest product launches in J&J’s history. Q2 will provide the first critical data points on market uptake and prescription volume.

- Oncology Volume Expansion: The expanded approval of TECVAYLI (in combination with DARZALEX FASPRO) for second-line multiple myeloma treatment is a major catalyst. Moving into earlier lines of therapy significantly increases the eligible patient population, sustaining double-digit growth in the oncology segment.

- Autoimmune Pipeline Progress: Following positive Phase 3 results for Nipocalimab (IMAAVY) in generalized Myasthenia Gravis (gMG), Q2 will focus on regulatory filings. This therapy is a cornerstone in J&J’s strategy to replace revenue lost to STELARA’s patent expiration.

2. MedTech: Technological Transition in Cardiovascular Care

- Shockwave and Abiomed Synergy: With the Shockwave Medical acquisition finalized, J&J now holds a unique leadership position in both heart recovery (Abiomed) and vascular calcification treatment (Shockwave). Q2 will see expanded cross-selling efforts across these high-growth platforms.

- PFA Adoption: The European rollout of the VARIPULSE Pro system is accelerating. This pulsed field ablation (PFA) technology is considered the future of atrial fibrillation treatment, and Q2 sales will reflect its success in challenging traditional thermal ablation methods.

- Digital Surgery Milestones: Updates on the OTTAVA robotic surgical platform are expected as the company prepares for its FDA submission. Progress here is a key indicator of J&J’s long-term competitiveness in digital health.

3. Financial and Operational Catalysts

- Raised Full-Year Guidance: The upward revision of total revenue guidance to 100.8B (midpoint) implies that Q2 must demonstrate strong operational resilience. Management is signaling confidence that its 28 platforms—each generating over 1B annually—can offset the 60%–70% volume decline expected for STELARA.

- Active Capital Allocation: J&J maintains a strong cash position. Management has indicated a continued appetite for “tuck-in” acquisitions, focusing on clinical-stage biopharmaceutical assets and high-growth med-tech technologies to bolster the 2027–2030 outlook.

Potential Challenges to Monitor

- Stelara Erosion Speed: The primary risk remains the pace at which biosimilars capture market share in the U.S. and Europe, which could impact gross margins if the transition happens faster than modeled.

- China Policy Continuity: Investors will be watching for any expansion of Volume-Based Procurement (VBP) into more advanced surgical consumables in the Chinese market during the second quarter.

Based on the Q1 2026 earnings report and market consensus, the earnings per share (EPS) for Johnson & Johnson (JNJ) is expected to show resilient growth over the next year, despite the headwinds from patent expirations.

The following is an analysis of the projected EPS trajectory:

EPS Forecast Data

The company has provided updated guidance, and market analysts have adjusted their expectations accordingly:

- Full-Year 2026 Guidance: J&J raised its adjusted EPS guidance to a range of $11.45–$11.65 (midpoint of $11.55). This represents an approximate 7.1% increase over 2025.

- Q2 2026 Estimate: Market consensus currently sits at approximately $2.87.

- Q3 2026 Estimate: Expectations rise to approximately $3.02 as new product launches gain traction.

- Full-Year 2027 Outlook: Analysts project a further climb to approximately $12.57, suggesting a growth rate of roughly 8.6% as the company moves past the initial peak of the STELARA patent cliff.

Primary EPS Drivers

- High-Margin Product Mix: The rapid scaling of oncology therapies like DARZALEX (growing at 18%+) and the launch of ICOTYDE (oral psoriasis peptide) are critical. These high-margin proprietary drugs are designed to replace the earnings power lost to biosimilar competition.

- MedTech Margin Expansion: The integration of Shockwave and Abiomed allows J&J to command premium pricing in the cardiovascular space. The transition to pulsed field ablation (PFA) with the VARIPULSE system is also expected to bolster segment profitability.

- Structural Efficiency: The ongoing restructuring of the Orthopaedics business is intended to streamline operations, allowing the company to focus resources on the higher-growth MedTech and Innovative Medicine segments.

Potential Headwinds to EPS

- The “Stelara” Erosion Curve: The most significant risk is the speed of biosimilar uptake. If STELARA sales decline faster than the projected 60%-70% volume erosion, it could lead to an EPS miss in the latter half of 2026.

- Financing and M&A Costs: Heavy acquisition activity (e.g., Shockwave) has increased interest expenses and amortization of intangible assets, which temporarily weighs on GAAP earnings.

- Pricing Pressures in China: The full impact of Volume-Based Procurement (VBP) on surgical supplies will be felt in late 2026, potentially squeezing MedTech margins more than currently modeled.

Overall, the sentiment remains positive, with the company expected to hit its $11.55 midpoint for 2026 and accelerate growth into 2027.

Source:

- https://www.investor.jnj.com/investor-news/news-details/2026/Johnson–Johnson-reports-Q1-2026-results-raises-2026-outlook/default.aspx

- https://www.investor.jnj.com/investor-news/news-details/2026/FDA-approval-of-ICOTYDE-icotrokinra-ushers-in-new-era-for-first-line-systemic-treatment-of-plaque-psoriasis-with-a-targeted-oral-peptide/default.aspx

- https://www.investor.jnj.com/investor-news/news-details/2026/Johnson–Johnson-Announces-64th-Consecutive-Year-of-Dividend-Increase-Raises-Quarterly-Dividend-by-3-1/default.aspx

- https://www.zacks.com/stock/news/2899644/johnson-johnson-jnj-q1-earnings-how-key-metrics-compare-to-wall-street-estimates

- https://seekingalpha.com/article/4890573-johnson-and-johnson-jnj-q1-2026-earnings-call-transcript

Back to J&J page