JPMorgan Chase (JPM) reported strong results for the first quarter of 2026, surpassing analyst expectations across key metrics. Below is the summary of the earnings analysis:

Core Financial Highlights

- Net Income: 16.5B, an increase of 13% year over year (YoY).

- Earnings Per Share (EPS): $5.94, beating the market consensus of $5.49.

- Managed Revenue: 50.5B, up 10% YoY, driven by growth across all business segments.

- Return on Tangible Common Equity (ROTCE): 23%, maintaining industry-leading profitability.

Segment Performance

- Corporate & Investment Bank (CIB): Revenue rose 19% to 23.4B. Investment banking fees surged 28% due to a rebound in M&A advisory and equity underwriting. Markets revenue hit a record 11.6B (up 20%).

- Asset & Wealth Management (AWM): Revenue grew 11% to 6.4B. Assets Under Management (AUM) reached $4.8 trillion (up 16%) following strong net inflows and market appreciation.

- Consumer & Community Banking (CCB): Revenue increased 7% to 19.6B, supported by higher credit card balances and loan growth.

- Payments: Revenue climbed 12% to 5.1B, marking its fifth consecutive quarterly record.

Key Trends and Outlook

- Net Interest Income (NII): While NII rose 9% to 25.5B this quarter, management slightly lowered the full-year 2026 NII guidance from 104.5B to approximately 103B. This reflects anticipated deposit pricing pressure and potential interest rate shifts.

- Credit and Expenses: The provision for credit losses was 2.5B, with net charge-offs at 2.3B. Non-interest expenses increased 14% to 26.9B, primarily due to higher compensation, technology investments, and front-office hiring.

- CEO Commentary: Jamie Dimon noted the strength of the economy but remains cautious regarding geopolitical tensions, the path of inflation, and evolving regulatory capital requirements.

Based on the 1Q26 financial results, several key shifts and dynamics shaped JPMorgan Chase’s performance this quarter:

1. Resurgence in Investment Banking and Markets

This was the most significant growth driver this quarter. Investment banking fees surged 28%, indicating that M&A and equity underwriting markets are recovering from previous lulls. Simultaneously, the Markets division achieved record revenue of 11.6B, benefiting from increased client activity and market volatility.

2. Cautious Outlook on Net Interest Income (NII)

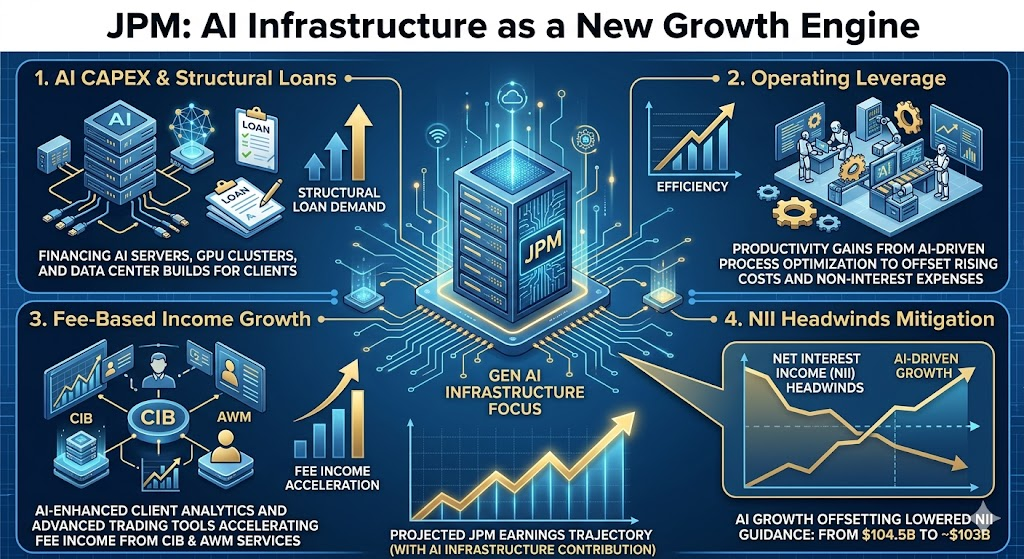

Although NII grew 9% to 25.5B this quarter, management lowered the full-year 2026 NII guidance from 104.5B to approximately 103B. This adjustment reflects expectations of rising deposit costs—as customers migrate funds to higher-yielding products—and potential shifts in the interest rate environment.

3. Record Assets Under Management (AUM)

AUM in the Asset & Wealth Management (AWM) segment reached a milestone of $4.8 trillion, up 16% YoY. This growth was driven not only by favorable market valuations but also by substantial net inflows, suggesting a “flight to quality” as clients seek stability in the current macro climate.

4. Continued Expansion of Operating Expenses

Total expenses rose 14% to 26.9B. The increase is primarily attributed to higher compensation, aggressive technology investments, and expanded front-office hiring. This indicates that despite strong profitability, JPM continues to reinvest heavily to maintain its competitive edge and digital capabilities.

5. Normalization of Credit Quality

The provision for credit losses stood at 2.5B. While consumer spending remains resilient, the rise in net charge-offs reflects a normalization of credit card delinquency rates from historically low levels. The firm maintains a cautious stance on macroeconomic risks and potential credit tightening.

Looking ahead to the second quarter of 2026 (Q2), JPMorgan Chase’s growth momentum is expected to shift from interest-rate dependency toward fee-based income and asset scale. Here are the primary drivers:

1. Sustained Recovery in Capital Markets (CIB)

The most anticipated growth engine for Q2 lies in Investment Banking. As the macroeconomic environment stabilizes, a pipeline of M&A deals and IPOs is expected to materialize. As a global leader, JPM is positioned to capture significant high-margin fee income. While the Markets division faces a high comparable base from last year, trading demand driven by geopolitical and policy shifts remains a potential upside.

2. Monetization of Record AUM (AWM)

The record $4.8 trillion in Assets Under Management (AUM) reached in Q1 will begin contributing full-quarter management fees in Q2. With continued strong net inflows and a generally optimistic outlook for global equities, the Asset & Wealth Management segment is projected to be one of the most stable profit contributors.

3. Expansion of Credit Card and Loan Balances (CCB)

The company expects the Card business to maintain strong growth momentum, projected at over 6%. Although Net Interest Margin (NIM) may face compression, the overall expansion in loan volume—including a recovery in mortgages and personal loans—will support the revenue base. Additionally, the Payments business is poised to mark its sixth consecutive record quarter, fueled by a rebound in e-commerce and global trade.

4. Structural Credit Demand from Infrastructure and AI

Management noted in recent updates that credit growth within the CIB and AWM sectors is being bolstered by strong demand for infrastructure development and AI-related capital expenditures. These structural CapEx trends are expected to translate into long-term loan growth.

5. Operating Leverage through AI and Technology

While expenses are rising due to hiring and R&D, the firm is aggressively integrating AI to enhance operational efficiency. Management expects AI initiatives to translate into significant productivity gains throughout 2026. If JPM successfully manages non-interest expenses in Q2, operating leverage could further expand profit margins.

Potential Challenges

- NII Headwinds: As customers continue to migrate funds into higher-yielding accounts, rising deposit costs (deposit repricing) may offset some revenue gains.

- Normalization of Credit Costs: A faster-than-expected rise in credit card delinquency rates could necessitate higher provisions for credit losses.

Based on current market consensus and analyst projections, JPMorgan Chase (JPM) is expected to maintain a trajectory of steady growth in Earnings Per Share (EPS) over the next year, though the growth rate may moderate compared to previous highs due to shifting interest rate dynamics.

1. Full-Year 2026 EPS Projections

Market analysts project JPM’s full-year 2026 EPS to fall between $21.88 and $22.28.

- Growth Rate: This represents an annual increase of approximately 8.5% to 13% compared to 2025.

- Quarterly Trends:

- Q1 Actual: $5.94 (outperforming the estimated $5.49).

- Q2 Forecast: The current consensus stands at approximately $5.46. While revenues are expected to remain high, Q2 EPS may be slightly lower than the Q1 peak due to seasonal expense patterns and rising funding costs.

2. Long-Term Outlook for 2027

Analysts remain optimistic for 2027, with a median EPS estimate of approximately $23.51.

- Upside Drivers: While Net Interest Income (NII) may face headwinds if the interest rate environment shifts, the robust recovery in Investment Banking (IB) fees and productivity gains from AI integration are viewed as the primary engines for profit growth in 2027.

3. Critical Factors Influencing EPS Direction

- NII Guidance Revision: The firm recently lowered its 2026 NII guidance from 104.5B to 103B. If deposit costs rise faster than anticipated—as customers move funds to seek higher yields—it will directly compress the upside potential for EPS.

- Capital Markets Momentum: The strong performance in IB fees (up 28% YoY) and Markets revenue (up 20% YoY) must persist to offset potential NII weakness. Continued activity in M&A and IPOs is the “X-factor” for EPS outperformance.

- Normalization of Credit Costs: The company currently forecasts a net charge-off rate of approximately 3.4% for credit cards. Any macro-economic deterioration that pushes delinquency rates significantly above this benchmark would act as a drag on EPS.

4. Analyst Sentiment and Valuation

- Average Price Target: Approximately $338.97.

- Investment Ratings: Over 70% of analysts maintain “Buy” or “Strong Buy” ratings, reflecting high confidence in JPM’s earnings resilience and its ability to navigate a complex macroeconomic landscape.

Source:

- https://www.jpmorganchase.com/content/dam/jpmc/jpmorgan-chase-and-co/investor-relations/documents/quarterly-earnings/2026/1st-quarter/a5fd2d13-877b-43b2-8b58-81bad4399c87.pdf

- https://mlq.ai/news/jpmorgan-chase-posts-strong-q1-2026-earnings-beating-expectations/

- https://www.alpha-sense.com/earnings/jpm/

- https://www.jpmorganchase.com/content/dam/jpmc/jpmorgan-chase-and-co/investor-relations/documents/2026-company-updates/company-update-firm-overview-transcript.pdf

- https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/investment-outlook/

- https://tickeron.com/ticker/JPM/forecasts-predictions/

- https://www.zacks.com/stock/quote/JPM/detailed-earning-estimates

- https://seekingalpha.com/symbol/JPM/earnings/estimates

- https://www.chartmill.com/stock/quote/JPM/analyst-ratings

Back to JPM page