1. The Memory Era & Birth of the Microprocessor (1968-1979)

Founded in 1968 by Robert Noyce and Gordon Moore (of Moore’s Law fame), Intel initially focused on semiconductor memory (SRAM and DRAM).

- 1971: Intel released the 4004, the world’s first commercially available microprocessor. Originally designed for a Japanese calculator company, it changed the course of computing.

- 1978: The launch of the 8086 processor established the x86 architecture, which remains the standard for most PCs and servers today.

2. The PC Revolution & “Intel Inside” (1980-1999)

Under the leadership of Andy Grove, Intel made the strategic “pivot of the century,” exiting the memory business to focus entirely on microprocessors as Japanese competitors flooded the RAM market.

- 1981: IBM chose the Intel 8088 for its first Personal Computer, cementing Intel’s dominance in the PC ecosystem.

- 1991: The “Intel Inside” marketing campaign launched, turning a hidden hardware component into a household brand name.

- 1993: The Pentium processor arrived, drastically increasing computing power and making multimedia PCs a reality for consumers.

3. The Core Era & The Tick-Tock Strategy (2000-2015)

This period was defined by intense competition with AMD and a shift from raw clock speed to power efficiency and multi-core processing.

- 2005: Steve Jobs announced that Apple would switch from PowerPC to Intel processors for all Mac computers.

- 2006: The Core microarchitecture was introduced, fixing the power and heat issues of the Pentium 4 era.

- Tick-Tock Model: Intel adopted a rigorous cadence—alternating between shrinking the manufacturing process (Tick) and updating the architecture (Tock) every year.

4. Manufacturing Stalls & Rising Competition (2016-2020)

Intel hit a “wall” with its 10nm manufacturing process, leading to years of delays while competitors like TSMC and Samsung surged ahead.

- Process Leadership Lost: For the first time, Intel lost its manufacturing lead, allowing AMD (using TSMC’s nodes) to gain significant market share with its Ryzen chips.

- Apple Silicon: In 2020, Apple announced it would ditch Intel for its own M-series chips, a major blow to Intel’s prestige in the premium laptop market.

- Data Center Shift: Despite PC struggles, Intel’s data center group became a massive profit engine as cloud computing exploded.

5. IDM 2.0 & The Comeback Trail (2021-Present)

With Pat Gelsinger returning as CEO, Intel launched its most ambitious turnaround plan to date.

- IDM 2.0 Strategy: Intel opened its doors to act as a foundry (Intel Foundry), manufacturing chips designed by other companies (like Amazon, Microsoft, and potentially Nvidia).

- 5 Nodes in 4 Years: A rapid roadmap to regain transistor leadership by 2025 with the Intel 18A node.

- The AI Pivot: With the rise of generative AI, Intel is pushing “AI PCs” (Meteor Lake and Lunar Lake) and trying to challenge Nvidia in the data center with its Gaudi accelerators.

Here is a competitive analysis of Intel’s market position as of 2026, focusing on its three primary battlefronts:

1. Data Center & AI: The Battle for the Silicon Throne

This is Intel’s most pressured segment, where it faces a “pincer movement” from GPU leaders and CPU challengers.

- The Nvidia Dominance: Nvidia’s CUDA software ecosystem remains a formidable moat. While Intel’s Gaudi 3 and future Falcon Shores accelerators offer better price-to-performance for specific AI workloads, they still struggle to match Nvidia’s developer mindshare in LLM training.

- AMD’s Market Share Erosion: AMD’s EPYC processors continue to gain ground in the server market. By leveraging TSMC’s advanced nodes earlier, AMD has maintained a lead in core density and energy efficiency (performance-per-watt).

- The Rise of Custom Silicon (ASICs): Cloud Service Providers (CSPs) like Google (TPU), Amazon (Trainium), and Microsoft (Maia) are designing their own chips. This reduces their reliance on Intel’s general-purpose Xeon CPUs.

2. Client Computing: Defending the PC Stronghold

Intel still leads the PC market by volume, but the architecture of the personal computer is shifting.

- The AI PC Arms Race: Intel’s Core Ultra (Lunar Lake/Arrow Lake) chips are in a fierce battle with AMD’s Ryzen AI series. Both are racing to integrate more powerful NPUs (Neural Processing Units) to handle local AI tasks.

- The ARM Threat: Apple Silicon (M-series) set a high bar for battery life and performance. Now, Qualcomm’s Snapdragon X Elite and other ARM-based Windows chips are challenging Intel in the premium laptop space, forcing Intel to radically improve its power efficiency.

3. Intel Foundry: The IDM 2.0 Gamble

Intel is attempting to become a world-class contract manufacturer, competing directly with the companies that currently produce chips for its rivals.

- TSMC (The Gold Standard): TSMC remains the leader in yield stability and ecosystem support. Intel’s goal is to achieve “PowerVia” and “RibbonFET” technologies with the Intel 18A node to leapfrog TSMC’s 2nm process by 2026.

- Samsung (The Direct Rival): Intel is effectively racing Samsung to be the “global number two” foundry. Both are competing for external orders from big players like Nvidia, Microsoft, and MediaTek to diversify their revenue beyond internal products.

Competitive Summary Table

| Segment | Primary Rivals | Intel’s Edge | Intel’s Weakness |

| AI Acceleration | Nvidia | Lower TCO (Total Cost of Ownership) | Weak software ecosystem compared to CUDA |

| Server CPU | AMD | Massive legacy enterprise install base | Lower core counts and efficiency vs EPYC |

| Consumer PC | Apple, Qualcomm | Deep OEM partnerships & x86 compatibility | Higher power consumption in mobile form factors |

| Foundry | TSMC, Samsung | US/EU domestic manufacturing & packaging | Unproven high-volume yields on leading-edge nodes |

Strategic Outlook

Intel’s success in 2026 hinges almost entirely on Intel 18A. If the 18A node achieves high-volume manufacturing success, Intel can regain the “transistor lead” it lost a decade ago, allowing its own products to be more competitive while simultaneously stealing high-margin foundry customers from TSMC and Samsung.

Source:

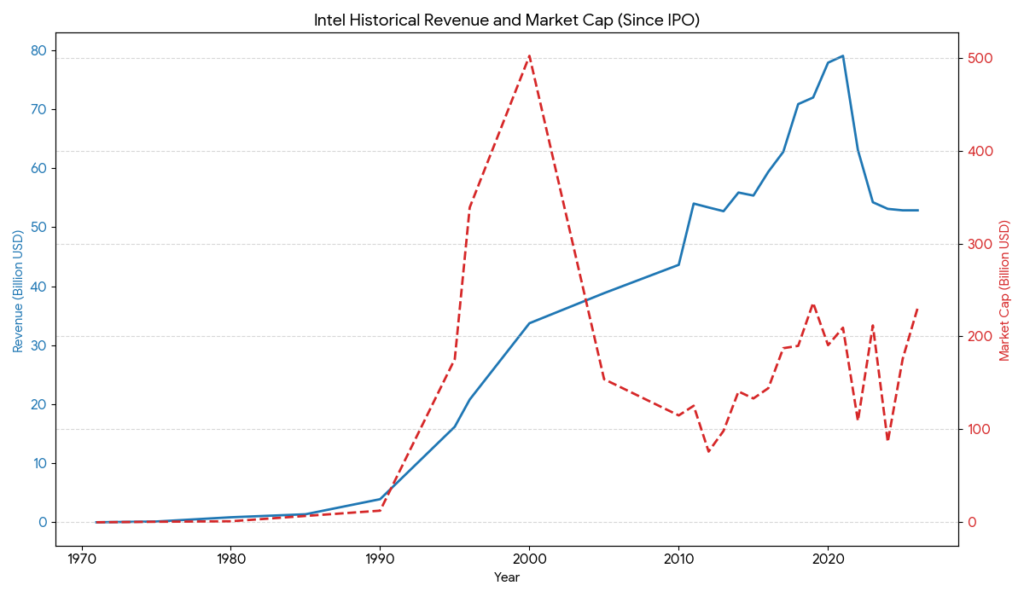

- https://www.macrotrends.net/stocks/charts/INTC/intel/revenue

- https://www.macrotrends.net/stocks/charts/INTC/intel/market-cap

- https://www.intc.com/financial-info/financial-results

- https://www.intel.com/content/dam/www/central-libraries/us/en/documents/2025-05/history-1971-annual-report.pdf

- https://www.youtube.com/watch?v=VMRk94Qc1a4

- https://www.intel.com/content/www/us/en/foundry/overview.html

- https://www.bloomberg.com/quote/INTC:US

- https://www.reuters.com/technology/intel-foundry-business-operating-losses-deepen-2024-04-02/

Back to Intel page