The history of Ping An Insurance reflects the rapid evolution of China’s financial sector. Its development can be categorized into five distinct strategic phases:

Phase 1: Exploration and National Expansion (1988–1994)

Ping An started as a pioneer, breaking the monopoly of state-owned insurance in China.

- 1988: Founded in Shekou, Shenzhen, as China’s first joint-stock insurance company.

- 1992: Formally adopted “China” in its name and began nationwide expansion; launched life insurance operations.

- 1994: Became the first Chinese financial institution to introduce foreign strategic investors, including Morgan Stanley and Goldman Sachs.

Phase 2: Professionalization and Diversification (1995–2002)

During this period, Ping An laid the groundwork for a broader financial services group.

- 1995–1996: Established Ping An Securities and Ping An Trust, marking the transition from a pure insurer to a financial group.

- 2002: HSBC became a major shareholder, bringing international management standards and technical expertise to the company.

Phase 3: Integrated Financial Services and Dual Listing (2003–2010)

This era was defined by the completion of its “Integrated Financial” architecture and capital market entries.

- 2004: Listed on the Hong Kong Stock Exchange (2318.HK).

- 2007: Listed on the Shanghai Stock Exchange (601318.SH).

- 2010: Acquired a controlling stake in Shenzhen Development Bank, which later merged to become the modern Ping An Bank, completing the group’s “Insurance, Banking, and Asset Management” pillars.

Phase 4: “Finance + Technology” Transformation (2011–2018)

Ping An pivoted to leverage technology to drive financial growth and incubated several “Unicorn” startups.

- 2011: Launched Lufax (https://www.google.com/search?q=Lu.com) to explore online wealth management.

- 2015: Formally introduced the “Finance + Technology” strategy, investing heavily in AI, Blockchain, and Cloud Computing.

- 2018: Ping An Good Doctor was listed in Hong Kong, signaling the group’s successful expansion into the healthcare ecosystem.

Phase 5: “Integrated Finance + Healthcare” and AI Deepening (2019–Present)

The current strategy focuses on high-quality growth through a dual-engine approach.

- Strategy Evolution: The focus has shifted to “Integrated Finance + Healthcare & Elderly Care,” integrating medical services with insurance products to create a closed-loop ecosystem.

- Life Insurance Reform: Since 2019, the group has undergone a massive structural reform of its life insurance channel, moving away from “quantity” to “quality” in its agent force.

- Digital Productivity: Utilizing proprietary AI for automated underwriting, claims processing, and personalized customer service.

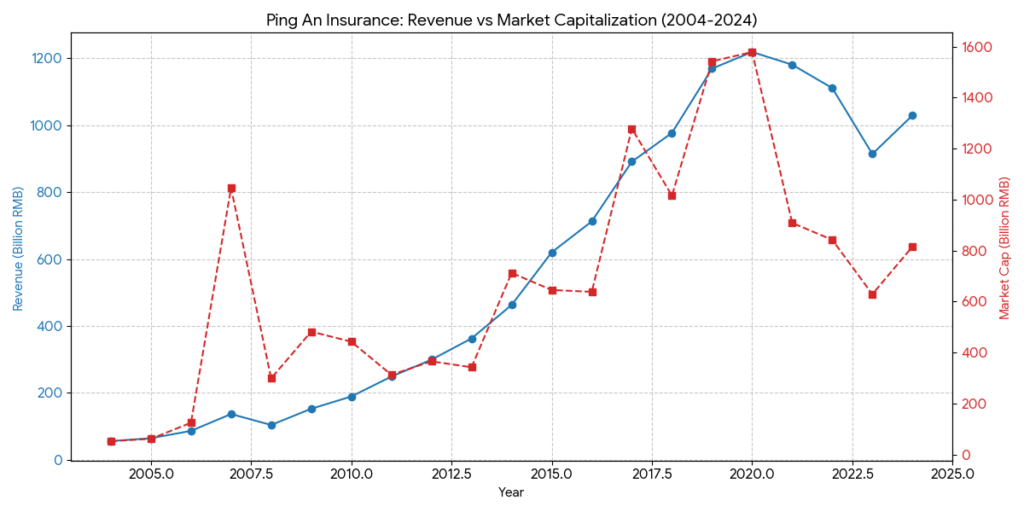

The recent decline in Ping An Insurance’s market capitalization is a result of a complex interplay between macroeconomic headwinds, specific sector exposures, and structural transitions within the company.

1. Exposure to the Real Estate Crisis

This has been the most significant drag on investor confidence.

- Asset Impairment: Ping An historically held large stakes in major Chinese developers (e.g., China Fortune Land, China Jinmao). As the property market cooled, Ping An had to recognize massive impairment provisions.

- Investment Risks: Investors remain cautious about the quality of the group’s underlying investment portfolio, fearing further hidden exposure to distressed commercial real estate assets.

2. Interest Rate Environment and “Negative Spread” Risk

- Lower Yields: China’s persistent low-interest-rate environment makes it difficult for life insurers to achieve the investment returns required to cover the guaranteed payout rates of older policies.

- Reinvestment Risk: As fixed-income assets mature, reinvesting that capital into new bonds with lower yields compresses long-term profit margins.

3. Structural Reform of Life Insurance

- Agent Force Downsizing: Ping An embarked on a massive “quality over quantity” reform, reducing its agent force from over 1 million to roughly 350,000–400,000 high-productivity professionals.

- Growth Transition: While the New Business Value (NBV) per agent has increased significantly, the overall volume contraction during this transition created a period of perceived stagnant growth.

4. Accounting Standard Volatility (IFRS 17 & 9)

- Revenue Recognition: The adoption of IFRS 17 changed how insurance revenue is recognized, making the top-line figures appear smaller and more volatile compared to previous years.

- Mark-to-Market Impact: Under IFRS 9, more investments are classified at fair value through profit or loss (FVTPL). This means short-term stock market fluctuations in China directly hit Ping An’s reported net profit, leading to higher earnings volatility.

5. Shift in Global Capital Allocation

- Foreign Outflows: As a heavyweight in the Hang Seng Index and MSCI China, Ping An is often the first stock sold when global institutional investors reduce their overall exposure to Chinese equities due to geopolitical tensions or macro-risk concerns.

In the 2025–2026 landscape, Ping An operates in a highly competitive environment where its “Integrated Finance” model is being challenged by both state-owned giants and agile tech firms.

1. Key Competitors by Sector

Ping An faces specialized competition across its three main pillars:

- Life Insurance: China Life (LPP). As the primary state-owned rival, China Life leverages its massive scale and government backing. In 2024–2025, China Life briefly surpassed Ping An in market cap due to its simpler, more stable investment profile during the property crisis.

- Property & Casualty (P&C): PICC P&C. This is Ping An’s toughest rival in auto and corporate insurance, holding a dominant market share through deep-rooted institutional relationships.

- Integrated Finance: CPIC (China Pacific Insurance) and NCI (New China Life). Both are aggressively copying Ping An’s “Insurance + Healthcare” playbook to boost customer stickiness.

- Fintech Disruption: Ant Group and Tencent (WeSure). These platforms compete for the younger demographic by offering frictionless, low-cost micro-insurance products.

2. Competitive Benchmarking (2025–2026 Projections)

| Metric | Ping An | China Life | CPIC |

| Brand Value (2026) | US$48.8B (Ranked #1 for 10 yrs) | ~US$17.5B | ~US$15.3B |

| NBV Growth (2025E) | High (+41.7%) | Steady/Moderate | Moderate |

| Combined Ratio (P&C) | 97.1% (Best-in-class efficiency) | N/A (Life focused) | 98.0% |

| R&D Investment | >1% of Revenue (Industry leading) | Moderate | Moderate |

3. Core Competitive Advantages (The “Moat”)

- Healthcare & Elderly Care Ecosystem: This is Ping An’s strongest differentiator. By integrating Ping An Good Doctor and Peking University Healthcare, it offers a “closed-loop” service. Data from 2025 shows that customers using both insurance and healthcare services have significantly higher retention and 2x higher profit contribution than insurance-only customers.

- Digital Productivity: Ping An’s AI handles 80% of customer service inquiries. Its AI-driven claims system has reduced the average auto claim processing time to 7.4 minutes, saving billions in fraud detection annually.

- Cross-Selling Engine: With ~250 million retail customers, nearly 40% hold more than one product within the group. This “one customer, multiple products” strategy keeps customer acquisition costs lower than peers who must buy traffic from external platforms.

4. Strategic Vulnerabilities

- Investment Sensitivity: Because Ping An’s portfolio is more diversified (including private equity and real estate), it experiences higher valuation volatility than China Life, which maintains a more “plain vanilla” bond-heavy portfolio.

- Market Share Pressure: During its multi-year agent reform, some market share in the “bancassurance” (bank-led insurance sales) channel was temporarily conceded to state-owned players like China Life and PICC.

Sources

- Ping An Official History Milestone

- Sina Finance: 1988-2013 Ping An Milestones

- Oreate AI Blog: Ping An’s 35-Year Journey

- DBS Bank: Ping An Insurance – Long-term re-entry point (2025)

- PR Newswire: Ping An Reports Operating Profit Recovery (9M 2025)

- Reuters: China’s Ping An faces property sector headwinds

- Brand Finance Global 500 2026 Report

- JPMorgan Research: 2026 Financial Services Sector Outlook

- Insurance Asia: China Life Premiums vs. Ping An NBV Projections

Back to Ping An Insurance page