The history of HDFC Bank can be divided into four primary stages, evolving from a startup in the mid-1990s to one of the most valuable banking institutions globally.

Phase 1: Foundation and Early Growth (1994–2000)

- 1994: Following India’s financial liberalization, HDFC Limited (the housing finance pioneer) received approval from the Reserve Bank of India (RBI) to set up a private sector bank.

- 1995: HDFC Bank commenced operations in January, with its first branch in Mumbai inaugurated by then-Finance Minister Manmohan Singh.

- 1995 March: Its Initial Public Offering (IPO) was oversubscribed 55 times, marking a strong start on the BSE and NSE.

- Focus: Initially, the bank focused on wholesale banking and corporate credit for top-tier Indian companies like Tata and Reliance to ensure high asset quality.

Phase 2: Strategic Mergers and Digital Birth (2000–2010)

- 2000: Acquired Times Bank, the first-ever merger of two private banks in India, which expanded its customer base significantly.

- 2001: Listed its American Depositary Receipts (ADRs) on the New York Stock Exchange (NYSE), gaining global visibility.

- 2008: Acquired Centurion Bank of Punjab (CBoP), which drastically increased its branch network and presence in Northern India.

- Digital Lead: This era saw the bank pioneering NetBanking and SMS banking, positioning itself as a technology-forward institution.

Phase 3: Retail Leadership and Systemic Importance (2010–2022)

- Market Dominance: Under the leadership of long-time CEO Aditya Puri, HDFC Bank became India’s most valuable bank, known for its low Non-Performing Asset (NPA) ratios.

- D-SIB Status: In 2017, the RBI designated HDFC Bank as a Domestic Systemically Important Bank (D-SIB), categorizing it as “too big to fail.”

- 2020: Aditya Puri retired, and Sashidhar Jagdishan took over as CEO, continuing the focus on digital transformation and rural market penetration.

Phase 4: The Mega-Merger and Global Giant (2022–Present)

- 2022 April: Announced a historic merger with its parent company, HDFC Limited, to consolidate India’s largest housing finance company with its largest private bank.

- 2023 July 1: The merger officially took effect. This $40 billion deal created a financial behemoth.

- Global Ranking: Post-merger, HDFC Bank became the world’s fourth-largest bank by market capitalization, trailing only JPMorgan Chase, ICBC, and Bank of America.

- Current Goal: The bank is now focused on cross-selling mortgage products to its massive banking customer base and expanding its physical footprint to over 13,000 branches.

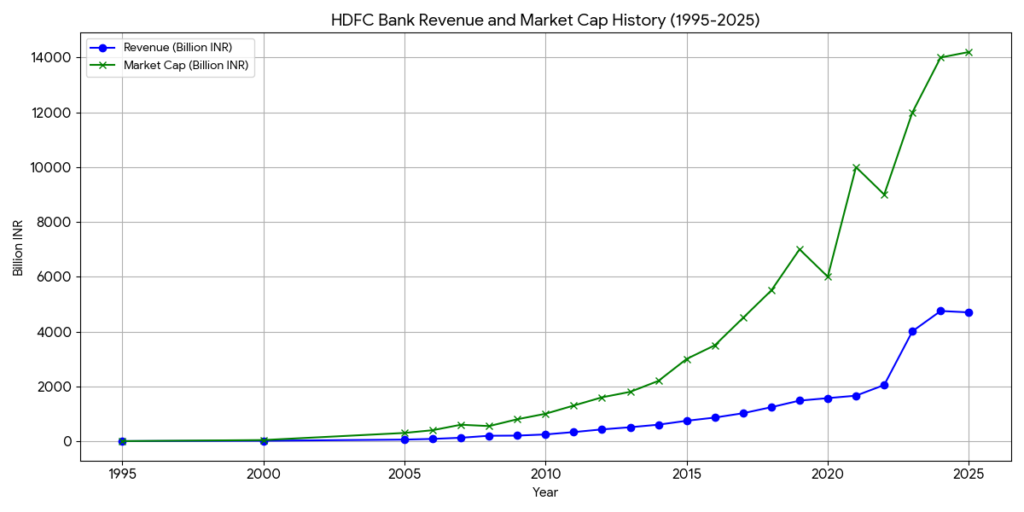

The reason HDFC Bank’s market capitalization (market value) has ascended much faster than its top-line revenue is a classic case of valuation premium. In the stock market, investors do not pay for revenue; they pay for quality of earnings, growth consistency, and risk management.

Here is an analysis of why the market assigns such a massive multiplier to HDFC Bank:

1. High Net Interest Margins (NIM)

In banking, revenue (interest income) is a “gross” figure. What matters to investors is the “spread” the bank keeps.

- HDFC Bank has historically maintained a NIM of 4% to 4.5%, which is significantly higher than most global peers (typically 2-3%).

- Market Logic: Because HDFC is more efficient at turning a dollar of deposits into profit, investors are willing to pay a much higher “Price-to-Sales” or “Price-to-Book” multiple compared to less efficient banks.

2. Best-in-Class Asset Quality

The biggest threat to a bank’s value is “bad loans” (Non-Performing Assets or NPAs).

- While many Indian public sector banks struggled with NPAs reaching 10-12%, HDFC Bank kept its Net NPAs consistently below 0.5% for decades.

- Risk Discount: In a risky industry like banking, a “clean” balance sheet is a rare commodity. Investors pay a scarcity premium for a bank that proves it can grow aggressively without losing money to defaults.

3. The “Compounder” Effect

Investors value HDFC Bank as a “secular growth story.”

- For over 20 years, the bank delivered a consistent 20% year-on-year profit growth.

- Valuation Multiplier: When a company proves it can grow predictably for decades, the market applies a lower “discount rate” to its future cash flows. This results in the stock price (and thus market cap) rising much faster than the current year’s revenue growth.

4. High Return on Assets (ROA)

HDFC Bank consistently generates an ROA of approximately 1.9% to 2.1%.

- Most global “G-SIBs” (Global Systemically Important Banks) struggle to maintain an ROA above 1%.

- Because HDFC Bank generates nearly double the profit from the same amount of assets as its global peers, its market cap reflects that superior productivity.

5. Institutional Scarcity & Index Weightage

- HDFC Bank is a “must-own” stock for any Foreign Institutional Investor (FPI) entering the Indian market.

- Following the 2023 merger with HDFC Limited, it became the heaviest weight in many Indian stock indices. This creates passive buying demand from ETFs, further pushing market cap higher regardless of immediate revenue fluctuations.

HDFC Bank operates in a highly competitive landscape, which can be categorized into three levels: Traditional Rivals, Public Sector Goliaths, and the Fintech Disruption.

1. The Battle of Private Giants (vs. ICICI & Axis)

The primary competition comes from other large private sector banks. While HDFC Bank is the market leader in market cap, ICICI Bank has closed the gap in terms of profitability metrics (ROA) over the last two years.

| Metric (Est. 2025) | HDFC Bank | ICICI Bank | Axis Bank |

| Market Cap (Billion INR) | ~14,240 | ~10,070 | ~4,270 |

| Loan Growth (YoY) | ~12-14% | ~15-16% | ~14% |

| Net Interest Margin (NIM) | ~3.4% – 3.6%* | ~4.3% – 4.5% | ~4.0% |

| Return on Assets (ROA) | ~1.9% – 2.0% | ~2.2% – 2.3% | ~1.7% – 1.8% |

Note: HDFC Bank’s NIM dropped slightly post-merger due to the higher cost of liabilities from HDFC Ltd, making efficiency a key battleground.

2. The Scale War (vs. State Bank of India)

State Bank of India (SBI) is the only bank larger than HDFC in terms of total assets and branch network.

- HDFC’s Advantage: Superior technology, faster loan processing, and better customer service for urban/middle-class segments.

- SBI’s Advantage: Massive “CASA” (Current Account Savings Account) base and a presence in every rural corner of India, providing them with the lowest cost of funds in the country.

- The Clash: HDFC Bank is currently aggressively expanding its rural branch network to challenge SBI’s dominance in deposit collection.

3. The Fintech & Shadow Banking Threat

Beyond traditional banks, HDFC Bank faces competition from agile digital players:

- Payments: PhonePe and Google Pay dominate the UPI ecosystem. While HDFC processes the backend, it has lost the “customer interface” for daily transactions.

- NBFCs (Shadow Banks): Bajaj Finance is a major competitor in consumer durable loans and personal financing, often offering faster digital approvals than traditional banks.

- Digital “Neo-banks”: Startups like Jupiter and Fi are targeting the Gen-Z demographic with superior UI/UX, forcing HDFC to overhaul its “PayZapp” and “MobileBanking” apps.

4. Strategic Moats (Competitive Advantages)

Despite the competition, HDFC Bank maintains several “Moats”:

- The “HDFC” Brand: Synonymous with trust and stability in India, allowing them to attract deposits even at lower interest rates than smaller rivals.

- Cross-Selling Engine: Following the merger, HDFC Bank has a massive opportunity to sell banking products to HDFC Ltd’s existing mortgage customers and vice versa.

- Data Advantage: With over 90 million customers, their proprietary credit scoring models are among the most advanced in the world, keeping default rates low.

Summary of Competitive Positioning

HDFC Bank is currently in a “consolidation and digestion” phase. Its main challenge is not just beating ICICI Bank, but successfully integrating the HDFC Ltd merger to lower its cost of funds and return to its historical 4%+ NIM levels.

Sources

- HDFC Bank Milestones: https://www.hdfcbank.com/personal/about-us/corporate-profile/milestones

- Wikipedia – HDFC Bank: https://en.wikipedia.org/wiki/HDFC_Bank

- Reuters – HDFC Merger News: https://www.reuters.com/business/finance/indias-hdfc-bank-completes-merger-with-parent-hdfc-2023-07-01/

- Jefferies Equity Research – India Banking Sector Outlook: https://www.jefferies.com/

- HDFC Bank Q3 FY25 Investor Presentation: https://www.hdfcbank.com/personal/about-us/investor-relations

- RBI Financial Stability Report 2025: https://www.rbi.org.in/

Back to HDFC page