History of Shell, categorized by stages:

1. The Origins and Shell Transport (1833–1890s)

Shell began not with oil, but with seashells. In 1833, Marcus Samuel opened a small shop in London selling antiques and Oriental seashells, which were popular for interior design at the time.

- 1891: His son, Marcus Samuel Jr., recognized the potential of exporting kerosene to the Far East.

- 1892: The Murex, the first oil tanker to pass through the Suez Canal, delivered 4,000 tons of Russian kerosene to Bangkok and Singapore.

- 1897: The Shell Transport and Trading Company was officially formed.

2. Merger with Royal Dutch (1907–1945)

To compete with the dominance of Rockefeller’s Standard Oil, Shell Transport merged with its rival, Royal Dutch Petroleum Company, in 1907.

- Ownership: Royal Dutch held 60% and Shell Transport held 40%.

- Global Growth: The group expanded rapidly into Russia, Romania, Venezuela, and Mexico.

- WWII: Shell became a vital supplier of fuel to the Allied forces, particularly high-octane aviation fuel and chemicals for explosives.

3. Post-War Expansion and Petrochemicals (1945–1970s)

Post-war reconstruction triggered a massive surge in energy demand. Shell entered a “golden age” of growth.

- Offshore Exploration: Shell pioneered deep-water drilling in the Gulf of Mexico and the North Sea.

- Diversification: The company invested heavily in chemicals, transforming crude oil into plastics and synthetic rubbers.

- 1970: Shell acquired full control of its U.S. subsidiary, strengthening its position in the American market.

4. LNG Leadership and Structural Changes (1980s–2010s)

Following the oil shocks of the 1970s, Shell pivoted toward natural gas and improved corporate efficiency.

- LNG Pioneer: Shell led the development of Liquefied Natural Gas (LNG) projects in Brunei and Australia, foreseeing gas as a cleaner alternative to coal.

- 2005: The complex dual-headed corporate structure was abolished. The company became a single entity, Royal Dutch Shell plc, headquartered in the Netherlands.

- 2016: Shell acquired BG Group for 50 billion pounds, making it the world’s largest producer of LNG.

5. Energy Transition and Rebranding (2021–Present)

Under increasing pressure to address climate change, Shell began its most significant transformation yet.

- 2021: Shell moved its headquarters from The Hague to London, simplified its share structure, and dropped “Royal Dutch” from its name to become Shell plc.

- Net Zero Strategy: The company set a target to become a net-zero emissions energy business by 2050.

- Current Focus: Shifting capital toward EV charging networks, hydrogen power, and carbon capture (CCS) while gradually reducing traditional oil production.

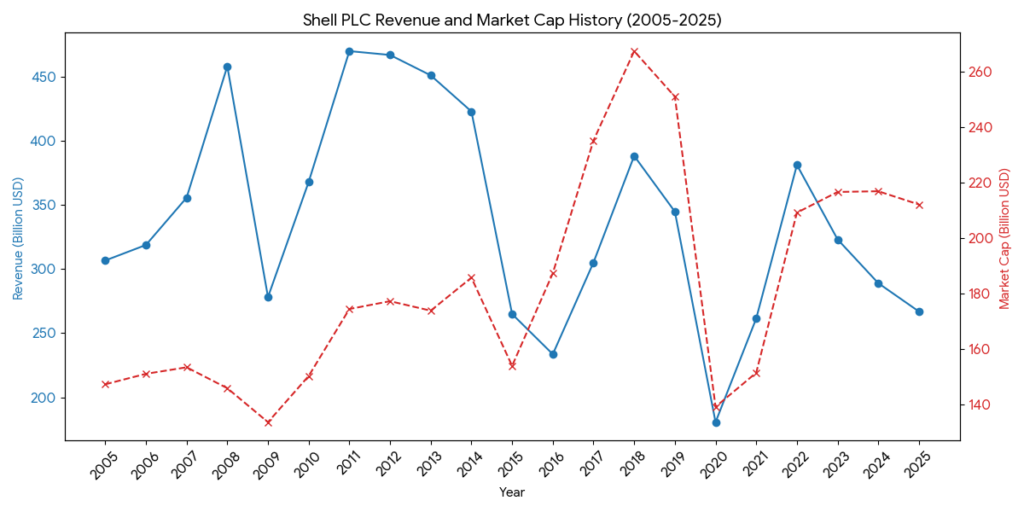

Shell PLC Revenue and Market Cap Analysis (2005–2025)

The chart illustrates the historical financial performance of Shell since its corporate unification in 2005. Key observations include:

- Revenue Volatility: Shell’s revenue is highly sensitive to global oil and gas price cycles. It peaked in 2011 at $470.17B during the commodity super-cycle. Significant dips occurred in 2015 (shale oil surge) and 2020 (COVID-19 pandemic), with the latter hitting a low of $180.54B.

- Market Cap Resilience: Despite revenue fluctuations, the market capitalization has remained relatively stable. It reached a high of $267.52B in 2018. In recent years (2022–2025), the market cap has stabilized above $210B, reflecting investor confidence in Shell’s transition toward LNG and renewable energy.

- The 2022 Recovery: Revenue surged back to $381.31B in 2022 due to the global energy supply crunch, which also helped the market cap recover from its pandemic lows.

Shell is currently focusing on “Value over Volume.” While it maintains a dominant position in the global gas market, it faces intense valuation pressure from its U.S. peers and execution risks in its chemicals division.

Here is the competitive analysis of Shell vs. the global “Supermajors”:

1. Financial & Market Positioning (2025–2026 Estimates)

| Metric | Shell | ExxonMobil (XOM) | Chevron (CVX) | TotalEnergies (TTE) |

| Market Cap (Billion) | ~$217 | ~$529 | ~$329 | ~$146 |

| P/E Ratio (NTM) | ~8.2x | ~12.5x | ~11.8x | ~7.5x |

| Primary Strength | LNG & Trading | Upstream Growth (Guyana) | Capital Discipline | Integrated Power |

| Dividend Yield | ~4.1% | ~3.4% | ~4.3% | ~4.8% |

2. Strategic Benchmarking

A. The Valuation Gap (Shell vs. U.S. Peers)

- The Problem: Shell (and BP) consistently trades at a discount compared to ExxonMobil and Chevron. Investors currently award higher premiums to U.S. companies for their aggressive oil production growth in low-cost basins like the Permian and Guyana.

- The Response: Shell CEO Wael Sawan has adopted “Commercial Realism,” cutting $5B–$7B in structural costs by 2028 to improve returns and narrow this gap. Shell is increasingly prioritizing high-margin deepwater projects (Brazil, Gulf of Mexico) over volume-heavy onshore assets.

B. The LNG Crown (Shell vs. TotalEnergies)

- Market Dominance: Shell remains the world’s largest LNG trader, a position bolstered by its 2016 BG Group acquisition. LNG acts as Shell’s “cash cow,” providing a bridge fuel as the world transitions away from coal.

- Competition: TotalEnergies is its fiercest rival here, following a similar “Gas + Electrons” strategy, but Shell’s integrated trading platform remains more sophisticated and profitable.

3. Key Competitive Advantages & Weaknesses

Advantages:

- Global Trading Prowess: Shell’s trading desk is a “black box” of profit, often generating billions during periods of high price volatility where others struggle.

- Deepwater Expertise: Shell is a leader in subsea technology, allowing it to extract oil at a lower breakeven (under $30/barrel in some offshore projects) compared to traditional peers.

Weaknesses:

- Chemicals Drag: Unlike Exxon, which has a highly integrated and profitable downstream sector, Shell’s chemicals business has been a laggard in 2025–2026, suffering from overcapacity and lower margins.

- Renewable Identity Crisis: Shell has scaled back on offshore wind and low-return solar projects to appease shareholders, but this risks falling behind TotalEnergies in the long-term race for “green” electrons.

4. 2026 Competitive Outlook

- Asset Monetization: Shell is aggressively divesting non-core assets (e.g., Nigerian onshore, Singapore refining) to focus on “high-grade” opportunities.

- Exploration Alpha: The success of the Namibia exploration (Orange Basin) is a critical competitive trigger. If Shell can commercialize these finds faster than TotalEnergies, it could significantly boost its upstream valuation.

Sources:

- https://www.reuters.com/business/energy/shell-exxon-bp-q4-2025-earnings-preview

- https://www.bloomberg.com/quote/SHEL:LN

- https://www.shell.com/investors/strategy-and-financial-targets.html

Back to Shell page