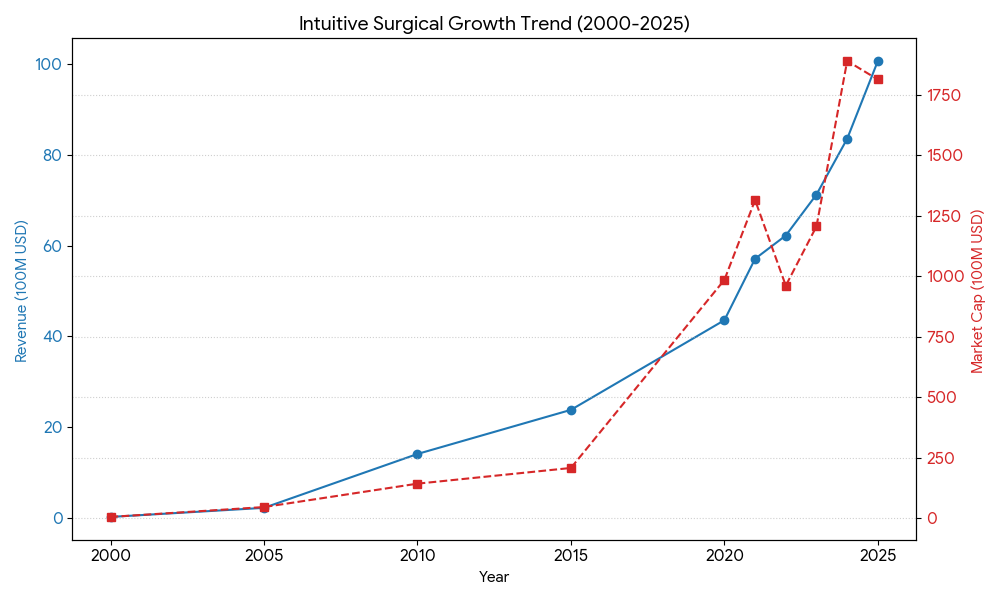

Here is the history of Intuitive Surgical (ISRG) categorized into four distinct development stages:

1995-2004: Foundations and Early Breakthroughs

This period was defined by the transition from military research to a commercial medical reality.

- 1995: Founded by Frederic Moll, Robert Younge, and John Freund. They acquired the license for robotic technology originally developed by SRI International for the U.S. Army.

- 2000: NASDAQ IPO and FDA Clearance. The original da Vinci system became the first robotic surgical system cleared by the FDA for general laparoscopic surgery.

- 2003: Merger with Computer Motion. After a long patent dispute, Intuitive acquired its main rival (maker of the ZEUS system), effectively consolidating the market and securing a massive patent portfolio.

2005-2013: Global Expansion and Technological Iteration

During this phase, the company refined its technology and proved its commercial viability globally.

- 2006: Launch of the da Vinci S. This second-generation system introduced 3D High-Definition (HD) visualization and streamlined the setup process.

- 2009: Launch of the da Vinci Si. This was a major leap forward, introducing “Dual Console” capability, which allowed two surgeons to work together or a senior surgeon to train a resident in real-time.

- Business Model Shift: The company perfected the “Razor and Blade” model, where the sale of the robot (system) was supplemented by recurring revenue from high-margin instruments (blades) and service contracts.

2014-2023: The Fourth Generation and Diagnostic Diversification

Intuitive moved toward multi-quadrant surgery and expanded its reach into diagnostics.

- 2014: Launch of the da Vinci Xi. This remains a flagship platform, featuring an overhead boom design that allows the robotic arms to rotate and reach any part of the patient’s body without moving the base.

- 2017-2018: Launch of the da Vinci X (a lower-cost version of the Xi) and the da Vinci SP (Single Port), which allows complex surgery through a single small incision.

- 2019: Launch of the Ion Endoluminal System. This marked a strategic pivot into diagnostics, specifically for minimally invasive peripheral lung biopsies to detect cancer early.

2024-Present: The Digital and AI Era

The current stage focuses on data-driven surgery and next-generation sensing.

- 2024: Launch of da Vinci 5. This fifth-generation platform features 10,000 times the computing power of the Xi. Its most significant innovation is Force Feedback technology, which lets surgeons “feel” the resistance of tissues for the first time in robotic history.

- Modern Milestones: Surpassing 17 million total procedures performed globally. The focus has shifted toward integrating AI, machine learning, and digital ecosystems to standardize surgical outcomes.

In the surgical robotics landscape, Intuitive Surgical (ISRG) continues to hold a dominant position, though it faces intensified competition as Medtronic and Johnson & Johnson move from regulatory hurdles to active market penetration.

Competitive Matrix (2026)

| Competitor | Core Platform | Market Strategy (2026) | Key Technical Edge |

| Intuitive Surgical | da Vinci 5 | Protects 80%+ share; focuses on AI and force-sensing tech. | Force Feedback: Surgeons can “feel” tissue resistance; 10,000x computing power. |

| Medtronic | Hugo RAS | Aggressive expansion in Europe/Asia; price-sensitive markets. | Modular Design: Individual arms on separate carts provide room flexibility. |

| Johnson & Johnson | Ottava | Post-FDA IDE approval (2024); starting major U.S. clinical trials. | Unified Ecosystem: Integrated with Ethicon instruments and Polyphonic digital platform. |

| Stryker | Mako | Dominates Orthopedics (>50% share); expanding to Spine/Shoulder. | Haptic Boundaries: Specialized for high-precision bone cutting and joint alignment. |

| CMR Surgical | Versius | Targets Ambulatory Surgery Centers (ASCs) and low-acuity cases. | Portability: Compact arms that can be easily moved between operating rooms. |

Deep Dive: Three-Way Battle for Soft Tissue Surgery

1. The Incumbent’s Moat: Intuitive Surgical (ISRG)

By early 2026, Intuitive has performed over 20 million procedures. Its competitive advantage is no longer just the hardware, but the Digital Ecosystem. The da Vinci 5 integrates AI that analyzes surgical video in real-time, comparing live data against millions of past cases to suggest optimal paths. The high “switching cost” for hospitals—driven by millions in investment and thousands of trained surgeons—remains their strongest defense.

2. The Modular Challenger: Medtronic (MDT)

The Hugo RAS system is gaining ground by addressing the “fixed cart” limitation of the da Vinci Xi. Because Hugo’s arms are modular, hospitals can use three arms for a simple urology case or four for a complex one, optimizing cost-per-procedure. In 2026, Medtronic is winning contracts in emerging markets where flexibility and lower consumable costs are prioritized over the highest-end AI features.

3. The Ecosystem Contender: Johnson & Johnson (J&J)

After years of delays, J&J’s Ottava is the most significant looming threat. Its unique design features six robotic arms integrated directly into the surgical table. This allows for a “zero-footprint” in the OR, a major selling point for overcrowded city hospitals. Furthermore, J&J leverages its massive existing sales network for surgical sutures and staplers (Ethicon) to bundle robotic systems with everyday hospital supplies.

2026 Industry Trends

- The Rise of Force Feedback: With da Vinci 5’s release, competitors are racing to add haptic/force-sensing capabilities, which were previously the biggest missing link in robotic surgery.

- Shift to ASCs: There is a rapid 16% CAGR growth in Ambulatory Surgery Centers. Companies are developing smaller, cheaper robots (like CMR Versius or Intuitive’s refurbished XiR) specifically for outpatient clinics.

- AI Integration: By 2026, “Robotic Surgery” is being rebranded as “Digital Surgery.” The focus is on predictive risk detection—the system alerting a surgeon before a nerve is nicked based on predictive mapping.

Sources:

- https://www.intuitive.com/en-us/about-us/company/history

- https://isrg.intuitive.com/news-releases/news-release-details/intuitive-announces-preliminary-fourth-quarter-and-full-year-2025-results

- https://www.macrotrends.net/stocks/charts/ISRG/intuitive-surgical/revenue

- https://news.medtronic.com/2025-12-03-Medtronic-announces-FDA-clearance-of-Hugo-TM-robotic-assisted-surgery-system-for-urologic-surgical-procedures

- https://news.medtronic.com/2026-02-17-Medtronic-announces-first-surgery-with-Hugo-TM-robotic-assisted-surgery-system-in-the-U-S-performed-at-Cleveland-Clinic

- https://www.jnj.com/media-center/press-releases/johnson-johnson-submits-ottava-robotic-surgical-system-to-the-u-s-food-and-drug-administration

- https://www.medtechdive.com/news/JJ-submits-FDA-de-novo-Ottava-robot-general-surgery/808976/

- https://isrg.intuitive.com/news-releases/news-release-details/da-vinci-5-cleared-cardiac-procedures/

- https://seekingalpha.com/news/4541889-intuitive-surgical-outlines-13-15-percent-da-vinci-procedure-growth-for-2026-as-global

Back to Intuitive Surgical page