The History of Citigroup: Key Stages

1. City Bank of New York (1812-1864)

The bank was founded in 1812 as the City Bank of New York, primarily to serve the merchants of New York City. During this early era, it played a vital role in financing the war effort during the War of 1812 and established itself as a cornerstone of New York’s growing commercial harbor.

2. National Expansion and Global Footprint (1865-1954)

- 1865: The bank joined the new U.S. national banking system and became The National City Bank of New York.

- 1894: It became the largest bank in the United States.

- 1914: Citi opened its first foreign branch in Buenos Aires, Argentina, marking the first time a U.S. national bank opened an overseas office.

- 1916: Through the acquisition of the International Banking Corporation (IBC), Citi gained a massive presence in Asia, including Shanghai and Hong Kong. In China, the bank became widely known as the “Starry Flag Bank” (花旗銀行) because of the American flag flying outside its offices.

3. Innovation and the Rise of “Citicorp” (1955-1997)

This era was defined by technological leadership and a shift toward consumer banking:

- 1955: A merger with First National Bank created First National City Bank of New York.

- 1967: The bank reorganized into a holding company called Citicorp.

- 1970s: Led by Walter Wriston, Citi revolutionized personal banking by rolling out 24-hour ATMs across New York, a move that changed how the world accessed cash.

- 1976: The bank officially shortened its name to Citibank.

4. The Megamerger and the Financial Crisis (1998-2020)

- 1998: In a historic $70 billion deal, Citicorp merged with Travelers Group to form Citigroup. This created a “financial supermarket” that combined banking, insurance, and investment services under one roof, effectively challenging the Glass-Steagall Act.

- 2008: The bank was hit hard by the subprime mortgage crisis. It required a massive federal bailout (TARP) to survive, leading to a period of downsizing and “de-risking” the balance sheet.

- 2010s: Citi focused on repaying the government and shedding non-core assets to return to its roots as a global corporate and investment bank.

5. Strategic Refocus (2021-Present)

- 2021: Jane Fraser became CEO, the first woman to lead a major Wall Street bank.

- Transformation: Under her leadership, Citi has been exiting consumer banking markets in Asia, Europe, and Mexico. The goal is to simplify the bank’s structure and focus on high-growth areas like Wealth Management, US Personal Banking, and Services for Institutional Clients.

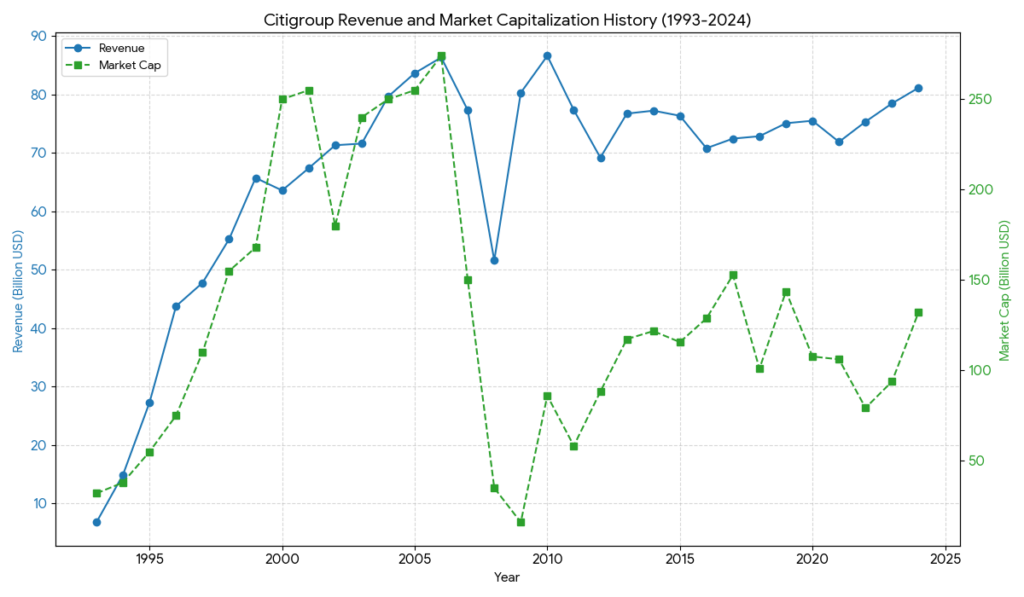

Citigroup Revenue and Market Capitalization History (1993-2024)

The chart illustrates the financial evolution of Citigroup from its growth years to the post-crisis transformation.

Key Observations:

- Growth and Merger Peak (1993-2006): Following the 1998 merger with Travelers Group, Citigroup’s market capitalization grew significantly faster than its revenue. By 2006, the market cap reached its all-time peak of approximately $274 billion, reflecting the market’s high valuation of the “financial supermarket” model.

- The Financial Crisis Impact (2007-2009): The subprime mortgage crisis led to a catastrophic collapse in market value. From its 2006 peak, the market cap plummeted to a low of approximately $16 billion in 2009. While revenue showed volatility but eventual stabilization due to government intervention and reporting adjustments, the market’s trust was severely shaken.

- Restructuring and Recovery (2010-2024): Since 2010, revenue has remained relatively stable in the $70 billion to $80 billion range. While the market cap has not returned to pre-2008 levels, it has seen a steady recovery. As of 2024, the market cap rose to approximately $132.19 billion, signaling investor confidence in the current strategic shift toward simplification and core institutional services.

In 2026, Citigroup’s competitive landscape is defined by its massive restructuring efforts. Unlike its peers who are expanding their footprints, Citi is deliberately shrinking to become a leaner, higher-returning institution focused on Services, Wealth, and Institutional Clients.

1. Peer Comparison: The “Big Four” in 2026

While JPMorgan Chase and Bank of America have focused on scaling their massive U.S. retail footprints, Citi has exited most of its international consumer markets to focus on corporate banking.

| Competitor | Core Strength | 2026 Market Position |

| JPMorgan Chase | Scale, Technology, M&A | The industry gold standard; leading in AI integration and digital banking. |

| Bank of America | Consumer Deposits, Wealth | Massive U.S. domestic base with strong synergy via Merrill Lynch. |

| Wells Fargo | U.S. Middle Market, Mortgages | Recovering market share after lifting of regulatory asset caps. |

| Citigroup | Global Services, Payments | The go-to bank for multinational corporations and global cross-border trade. |

2. Strategic Advantages (The “Citi” Edge)

- Treasury and Trade Solutions (TTS): Citi’s “crown jewel.” It manages the global supply chain payments for 90% of Fortune 500 companies. In 2026, this high-margin, recurring revenue stream is Citi’s primary defense against competitors.

- The Transformation Catalyst: Citi is currently undergoing its most significant reorganization in 20 years. By 2026, it aims to reduce its workforce by 20,000 and exit nearly all non-core international consumer businesses (including the Banamex IPO in Mexico).

- Valuation Gap: Citi historically trades at a discount compared to its book value. In 2026, as ROTCE (Return on Tangible Common Equity) trends toward its 11%-12% target, analysts see it as a “re-rating” candidate with more upside potential than the already highly-valued JPMorgan.

3. Financial Performance Comparison (2026 Outlook)

- Return on Equity (ROE): JPMorgan remains the leader (>15%), but Citi is showing the fastest rate of improvement as it sheds low-return assets.

- Efficiency Ratio: Citi is aggressively targeting a ratio below 60% by 2026. This is the key metric investors are watching to see if the management can successfully lower the cost of doing business.

- Capital Returns: With a simplified structure, Citi has increased its share buybacks in 2025 and 2026, returning more capital to shareholders relative to its market cap than its more “expensive” peers.

4. Critical Risks & Challenges

- Regulatory Consent Orders: Unlike its peers, Citi is still under heavy scrutiny from the Fed and OCC to fix its legacy data and risk management systems. The cost of compliance remains a drag on earnings.

- Execution Risk: The “New Citi” depends entirely on the successful integration of its five new business segments. Any delay in the sale of overseas assets could hurt 2026 earnings projections.

Sources:

Back to Citigroup page