The Royal Bank of Canada (RBC) dates back to 1864. It has evolved from a local bank serving East Coast merchants into one of the largest banks in the world. Its development can be divided into the following five key stages:

1. The Formative Years (1864–1900)

The core of this period was the transition from a local private partnership to a public chartered bank.

- 1864: Eight merchants in Halifax founded its predecessor, Merchants Bank of Halifax, originally to support local maritime trade (such as sugar and rum).

- 1869: Obtained a federal charter and was formally incorporated with an initial capital of $300,000.

- 1882: Began international expansion by opening its first overseas branch in Bermuda, primarily due to frequent trade between Halifax and the West Indies.

- 1893: Listed on the Montreal Stock Exchange.

Core Products: Bill discounting, letters of credit for maritime trade (sugar, timber, fish), and gold trading.

Core Strategy: Merchant-Centric Growth. Following the trade routes of Halifax merchants to the West Indies to provide financing where competitors were absent.

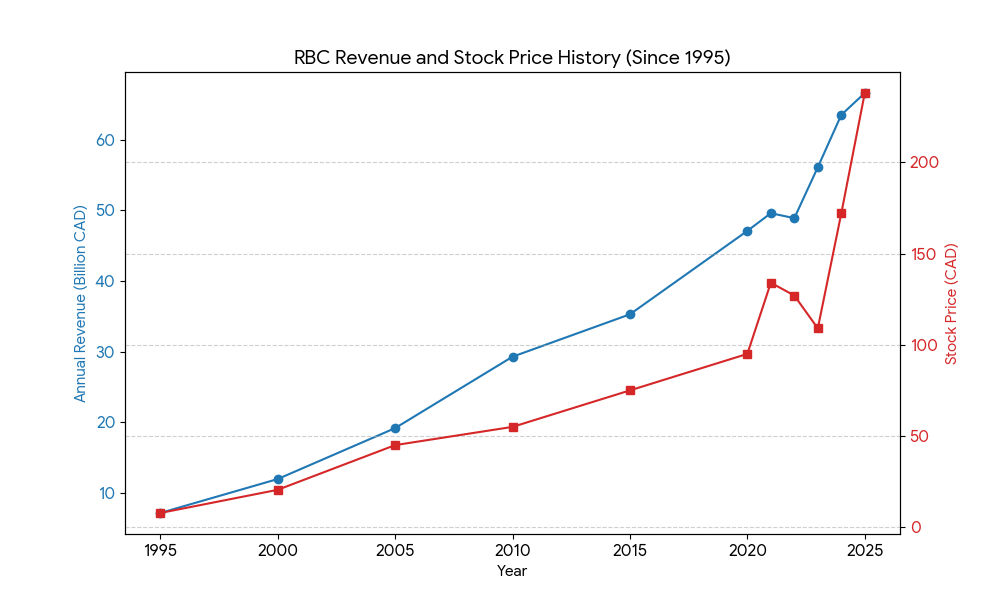

Revenue/Scale: Started with $300,000 in capital in 1869. By 1900, assets reached $18 million, reflecting a stable regional operation.

2. Rebranding and National Expansion (1901–1930)

During this stage, the bank changed its name and moved its focus to Canada’s financial center, growing rapidly through acquisitions.

- 1901: Formally renamed Royal Bank of Canada (RBC) to reflect its cross-regional business nature.

- 1907: Moved its headquarters from Halifax to Montreal, entering the financial hub of Canada at the time.

- 1925: Acquired Union Bank of Canada, a landmark event that made RBC the largest bank by asset size in Canada.

- 1929: Assets surpassed $1B for the first time, making RBC the first Canadian bank to reach this milestone.

Core Products: Savings accounts, agricultural loans (supporting the Western Canada settlement), and commercial lending.

Core Strategy: The “National Bank” Blueprint. Moving the HQ to Montreal and aggressively acquiring smaller banks (e.g., Union Bank of Halifax) to build a coast-to-coast network.

Revenue/Scale: In 1929, RBC became the first Canadian bank to surpass $1 billion in total assets, establishing it as the largest bank in the country.

3. Technical Innovation and Modern Transformation (1931–1980)

After World War II, RBC began to lead the market using technology and product innovation.

- 1935: Pioneered the first drive-in teller service in Canada.

- 1958: Entered the Asian market by establishing a representative office in Hong Kong.

- 1961: Became the first Canadian bank to install a computer system (IBM 1401) to handle administrative operations.

- 1976: Due to political and economic shifts in Quebec, the headquarters’ administrative functions were moved from Montreal to Toronto.

Core Products: Personal mortgages (post-1954 Bank Act changes), energy sector financing (oil & gas), and consumer credit.

Core Strategy: Operational Efficiency & Sector Expertise. Investing in early mainframe computers (1961) to handle the explosion of retail accounts and creating specialized divisions for the burgeoning energy industry.

Revenue/Scale: Assets grew from $2.5 billion in 1950 to over $60 billion by 1980, driven by the post-WWII economic boom.

4. Diversification and Financial Group Consolidation (1981–2010)

As financial regulations were relaxed, RBC transformed from a single bank into a comprehensive financial group.

- 1987: Acquired Dominion Securities, significantly strengthening its investment banking (Capital Markets) capabilities.

- 1993: Acquired Royal Trust, then the largest trust company in Canada, expanding its wealth management footprint.

- 2001: Unified its brand identity under “RBC,” establishing divisions such as RBC Royal Bank, RBC Capital Markets, and RBC Wealth Management.

- Early 2000s: Conducted a series of acquisitions in the US (such as Centura Banks), but sold its US retail operations in 2011 due to integration challenges.

Core Products: Investment banking (M&A, IPOs), wealth management, mutual funds, and insurance.

Core Strategy: The “One RBC” Integrated Model. Transitioning from a traditional lender to a financial supermarket. This was achieved by acquiring Dominion Securities (1987) and Royal Trust (1993) to capture higher-margin fee income.

Revenue/Scale: By 2010, annual revenue reached approximately $28 billion CAD, with a net income of $5.2 billion CAD.

5. Global Wealth Management and Strengthening Leadership (2011–Present)

In recent years, RBC has focused on high-net-worth wealth management and strategic large-scale acquisitions.

- 2015: Acquired the US-based City National Bank (known as the “Bank to the Stars”) for $5B, successfully re-entering the US high-end commercial and personal banking market.

- 2022: Acquired British wealth management firm Brewin Dolphin, strengthening its presence in the UK and Ireland.

- 2024: Completed the acquisition of HSBC Bank Canada for $13.5B. This was the largest bank merger in Canadian history, further consolidating its leadership position in the domestic market.

Core Products: High-net-worth private banking, AI-driven digital platforms, and cross-border commercial banking.

Core Strategy: Strategic Scale & Technology. Focusing on high-ROE (Return on Equity) businesses like wealth management (buying City National in 2015 and Brewin Dolphin in 2022) and massive domestic consolidation (buying HSBC Canada in 2024).

Revenue/Scale: 2024 Revenue: ~$57 billion CAD. Net Income: $16.2 billion CAD. Total assets have now surpassed $2 trillion CAD, making it the 10th largest bank globally by market cap.

In 2026, the Royal Bank of Canada (RBC) maintains its position as the “King of Canadian Banking,” serving as the benchmark for stability and performance. However, the competitive landscape has shifted due to major acquisitions and regulatory challenges faced by its peers.

1. Traditional Peer Comparison (The “Big Five”)

RBC continues to lead in nearly all financial metrics, particularly following its $13.5 billion acquisition of HSBC Canada in 2024, which significantly boosted its international and high-net-worth client base.

| Competitor | 2026 Competitive Status | Key Differentiator vs. RBC |

| TD Bank | Recovering. Still managing the fallout from 2024-2025 U.S. regulatory issues and money laundering fines. | Focuses on U.S. retail growth (East Coast) and customer service convenience (longer hours). |

| Scotiabank | Refocusing. Shifting capital from high-risk emerging markets to North American corridors (Canada-U.S.-Mexico). | Highest dividend yield among peers; attracts income-focused value investors. |

| BMO | Challenger. Strong momentum in commercial lending and ETFs. | Stronger emphasis on mid-market commercial banking in the U.S. Midwest (Bank of the West). |

| CIBC | Specialist. High concentration in Canadian mortgages and domestic retail. | Strongest digital mobile experience scores among traditional banks. |

2. Core Competitive Advantages in 2026

- Scale & Synergy: As the 11th largest bank globally, RBC benefits from a lower cost of funding. The HSBC integration has added roughly CAD $214 million in quarterly net income, creating a gap in market share that peers struggle to close.

- AI Enterprise Value: RBC’s strategic AI initiative (via Borealis AI) is on track to generate $700 million to $1 billion in enterprise value by 2027 through fraud detection and hyper-personalized wealth advice.

- Dominant Capital Markets: RBC Capital Markets revenue is more than double the Canadian peer average, controlling nearly 40% of the domestic M&A and debt underwriting market.

3. RBC vs. TD: The Battle for North America

The competition between RBC and TD has diverged significantly in 2026:

- RBC Strategy: Prefers Wealth Management and Commercial Banking in the U.S. (City National Bank). It targets high-margin, capital-light advisory fees.

- TD Strategy: Historically focused on Retail/Branch Banking. However, TD’s recent regulatory constraints in the U.S. have allowed RBC to gain ground in cross-border wealth services.

4. SWOT Analysis Summary (2026 Outlook)

Strengths: Diversified revenue (Banking, Wealth, Insurance, Capital Markets); #1 Brand Trust in Canada.

Weaknesses: High fee structure compared to digital-only banks (e.g., EQ Bank, Wealthsimple).

Opportunities: Further U.S. wealth management acquisitions; expansion into “Net-Zero” transition financing.

Threats: Slower GDP growth in Canada (forecasted at 0.7% for 2026); rising competition from Fintechs in the payments sector.

Source:

- RBC History – 150 Years of Innovation

- The Canadian Encyclopedia – RBC History

- RBC 2024 Annual Report

Back to RBC page