Stage 1: The SaaS Disruptor (1999-2004)

The focus during this period was challenging the traditional software model.

- 1999: Marc Benioff and three co-founders started Salesforce in a San Francisco apartment with the goal of making business software as easy to use as Amazon.

- 2000: Launched the famous “No Software” marketing campaign, directly challenging industry giants like Siebel.

- 2003: Hosted the first Dreamforce conference, establishing its unique community culture.

- 2004: Went public on the NYSE (IPO), raising 110 million dollars.

Core Product: Sales Cloud (Initial CRM).

Core Strategy: “No Software” Movement. Revolutionizing the industry by offering software as a service (SaaS) through a web browser, eliminating the need for expensive hardware and complex installations.

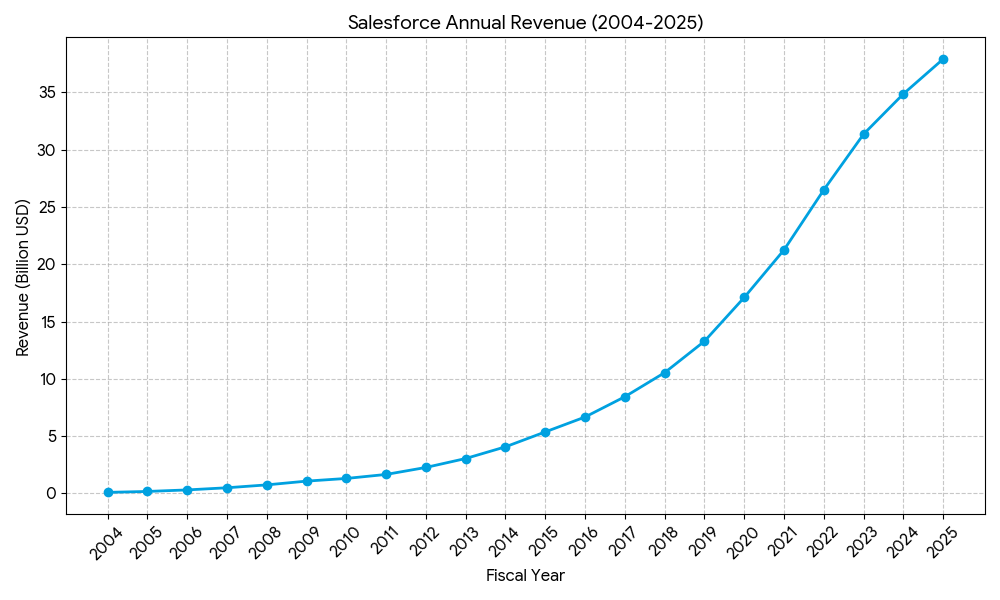

Revenue Level: Rapid early-stage growth. Revenue rose from $5.4 million in 2001 to approximately $96 million by its IPO in 2004, maintaining a nearly 100% year-over-year growth rate.

Stage 2: PaaS and Ecosystem Building (2005-2015)

Salesforce realized a single product couldn’t meet every need and pivoted toward becoming a platform.

- 2005: Launched AppExchange, often called the “eBay of enterprise software,” creating a third-party app ecosystem.

- 2007: Introduced Force.com (now Salesforce Platform), pioneering PaaS (Platform as a Service) by allowing developers to build apps directly in the cloud.

- 2009-2013: Expanded via acquisitions and internal development to launch Service Cloud (2009) and Marketing Cloud (2012).

- 2014: Launched Trailhead, gamifying the learning experience for complex enterprise software.

Core Product: AppExchange, Force.com (now Salesforce Platform), and Service Cloud.

Core Strategy: Platform as a Service (PaaS). Shifting from a single-app vendor to a platform provider. By launching AppExchange, they created an ecosystem where third-party developers could build and sell apps, significantly increasing customer stickiness.

Revenue Level: Scaling into the billions. Revenue grew from $176 million in 2005 to $5.37 billion in 2015, establishing its dominance in the cloud sector.

Stage 3: Expansion through Big Data and AI (2016-2022)

This phase focused on data integration and massive acquisitions to extend into collaboration and analytics.

- 2016: Introduced Einstein AI, embedding artificial intelligence into CRM workflows. Acquired Demandware to enter the e-commerce space (Commerce Cloud).

- 2018: Acquired MuleSoft for 6.5 billion dollars to solve data integration challenges across enterprise silos.

- 2019: Acquired Tableau, a leader in data analytics, for 15.7 billion dollars to enhance data visualization.

- 2021: Completed the 27.7 billion dollars acquisition of Slack, positioning it as the “Digital HQ” for businesses.

Core Product: MuleSoft (Integration), Tableau (Analytics), and Slack (Collaboration).

Core Strategy: The “Digital HQ” and Data Integration. Utilizing massive acquisitions to break down data silos within enterprises. The goal was to provide a 360-degree view of the customer by combining sales data with analytics, integration, and communication tools.

Revenue Level: Explosive expansion through M&A. Revenue climbed from $8.4 billion in 2017 to $26.5 billion in 2022.

Stage 4: The Agentic AI Revolution (2023-Present)

With the explosion of generative AI, Salesforce has shifted to an “Agent-first” strategy.

- 2023: Launched Einstein GPT and AI Cloud, combining generative technology with customer data.

- 2024: Introduced Agentforce, marking the transition from “Copilots” to “Autonomous Agents” that can execute tasks independently rather than just offering suggestions.

Core Product: Data Cloud, Einstein GPT, and Agentforce.

Core Strategy: Agent-first AI. Transitioning from “Copilots” (assistants) to “Autonomous Agents” (Agentforce) that can perform tasks independently. Data Cloud serves as the critical engine, unifying company data to power these AI agents effectively.

Revenue Level: Mature, steady growth. Revenue reached $34.9 billion in 2024 and is projected to surpass $41 billion in 2026.

In the 2026 market landscape, Salesforce remains the dominant force in CRM, but the nature of competition has shifted from “features” to “data intelligence” and “autonomous action.”

1. Market Share Landscape (2025-2026)

Salesforce maintains a substantial lead with approximately 22-23% of the global CRM market. However, its “moat” is being tested by Microsoft’s aggressive ecosystem bundling and the rise of AI-native challengers.

| Vendor | Approx. Share | Strategic Moat |

| Salesforce | 22% | Deep industry-specific clouds, vast AppExchange ecosystem, and Agentforce. |

| Microsoft | 8-10% | Seamless integration with Azure, Teams, and M365; aggressive Copilot pricing. |

| Oracle | 4-5% | Strong back-office ERP integration and high-performance database roots. |

| SAP | 3.5% | Dominance in global supply chain and complex manufacturing operations. |

| Others (HubSpot, etc.) | 50%+ | Lower complexity, faster time-to-value for Mid-Market/SMEs. |

2. Deep Dive: Key Competitors

Microsoft (The Ecosystem Challenger)

- The Threat: Microsoft’s Dynamics 365 is Salesforce’s most formidable rival. By leveraging “E5” licensing bundles, Microsoft makes it financially difficult for enterprises to justify the extra cost of Salesforce.

- AI Pivot: While Microsoft focuses on Copilot (enhancing human productivity within Office apps), Salesforce is betting on Agentforce (replacing manual workflows with autonomous agents).

HubSpot (The Mid-Market Disruptor)

- The Threat: HubSpot has successfully moved “up-market.” It wins on User Experience (UX). While Salesforce is often viewed as a complex system that requires expensive consultants, HubSpot is seen as “built, not bought,” offering a unified codebase that is easier to manage.

- Segment: Increasingly winning over Salesforce’s smaller and mid-sized accounts.

Oracle & SAP (The Vertical Defenders)

- The Threat: They own the ERP (Enterprise Resource Planning) layer. For heavy industries where CRM data must sync perfectly with inventory, finance, and supply chain, these incumbents use “Data Sovereignty” and “Single Source of Truth” arguments to keep Salesforce out of their accounts.

3. The New Battlefield: Copilots vs. Autonomous Agents

The competitive narrative in 2026 has evolved from who has the best UI to who has the most reliable AI Agents.

- Salesforce’s “Agentforce” Strategy: Aims to prove that AI can handle customer service or lead qualification without human intervention, justifying its premium price through labor savings.

- The Tech Stack Competition: Competition is moving down the stack. Salesforce is now competing with Snowflake and Databricks via its Data Cloud, as the quality of AI output is now entirely dependent on how well-integrated the underlying data is.

4. Competitive Risks for Salesforce

- Complexity & Total Cost of Ownership (TCO): Salesforce often requires dedicated “Admins” and developers. Competitors are gaining ground by offering “No-code” AI configurations that reduce the need for specialized headcount.

- Platform Fatigue: After years of acquisitions (Slack, Tableau, MuleSoft), some customers feel the platform has become fragmented. Competitors like Microsoft offer a more “native” feel across their suite.

Strategic Summary:

Salesforce’s survival as the leader depends on Data Cloud. If Salesforce can convince enterprises that it is the only platform capable of unifying “trapped” data to power autonomous AI, it will maintain its premium valuation. If CRM data becomes a commodity that can be easily queried by any AI (like OpenAI or Microsoft), Salesforce’s moat will shrink.

Sources:

Back to Salesforce page