Merck History: Key Phases (English Version)

The history of Merck is unique because it involves two distinct global entities: Merck KGaA (Germany) and Merck & Co. (USA/Canada, known as MSD elsewhere). Here is the chronological breakdown of their evolution:

Phase 1: The Pharmacy Roots & Industrialization (1668–1890)

Merck is the world’s oldest operating chemical and pharmaceutical company.

- 1668: Friedrich Jacob Merck purchased the “Angel Pharmacy” (Engel-Apotheke) in Darmstadt, Germany. This became the foundation of the family business.

- 1827: Heinrich Emanuel Merck transitioned the pharmacy into an industrial enterprise. He began the mass production of alkaloids like morphine and quinine, establishing high purity standards.

- 1887: Merck opened a sales office in New York to expand into the American market.

Core Products: Morphine, Quinine, Strychnine, and various alkaloids.

Core Strategy:

- Transitioning from a family-run pharmacy (“Angel Pharmacy”) to a large-scale industrial chemical factory.

- Pioneering the “Purity Guarantee,” ensuring that chemicals met consistent scientific standards for medical use.

Revenue Level: Transitioned from a local business to a major European chemical supplier; revenue was measured in millions of Goldmarks.

Phase 2: Expansion and the Great Split (1891–1945)

World War I changed the company’s structure forever, leading to the creation of two independent firms.

- 1891: George Merck (grandson of Heinrich Emanuel) established Merck & Co. in the United States as a subsidiary.

- 1917 (WWI): Following the U.S. entry into World War I, the American subsidiary was confiscated by the U.S. government. It was later re-established as an independent American company, completely separate from the German parent.

- Post-War Legalities: The two companies reached agreements on name usage.

- Merck KGaA (Germany): Holds the rights to the name “Merck” globally, except in the U.S. and Canada (where it operates as EMD).

- Merck & Co. (USA): Holds the rights to the name “Merck” in the U.S. and Canada, but operates as MSD (Merck Sharp & Dohme) in the rest of the world.

Core Products: * Germany: Fine chemicals, vitamins, and laboratory reagents.

- USA (MSD): Penicillin, Streptomycin (antibiotics), and Vitamin B12.

Core Strategy:

- Germany: Focused on maintaining European market dominance while surviving the hyperinflation and destruction of two World Wars.

- USA (MSD): Rapidly industrializing antibiotic production to support WWII efforts and establishing legal independence from the German parent.

Revenue Level: * Germany: Highly volatile due to war losses and economic collapse in Germany.

- USA (MSD): Steady growth, reaching the hundreds of millions of USD as it became a cornerstone of the U.S. pharmaceutical industry.

Phase 3: The Era of Blockbusters and Vaccines (1950–2000)

Both companies became giants in modern medicine through independent R&D.

- Merck & Co. (MSD):

- 1953: Merged with Sharp & Dohme, strengthening its position in the U.S.

- 1980s: Launched the world’s first statin (Mevacor) to treat high cholesterol.

- Vaccine Leadership: Developed groundbreaking vaccines for Measles, Mumps, and Hepatitis B.

- Merck KGaA (Germany):

- Liquid Crystals: While maintaining a pharma presence, they became the global leader in Liquid Crystal (LC) materials used in modern screens and displays.

- 1995: The company went public on the Frankfurt Stock Exchange, though the Merck family remains the majority owner.

Core Products: * Germany: Liquid Crystals (LC) for displays, Gonal-f (fertility), and Erbitux (oncology).

- USA (MSD): Mevacor/Zocor (statins), Vasotec (blood pressure), and Hepatitis B vaccines.

Core Strategy:

- Germany: Pursued a “Hybrid” model, diversifying into high-tech materials (Liquid Crystals) to balance the risks of drug development.

- USA (MSD): Adopted the “Blockbuster” strategy, investing heavily in R&D to find high-volume drugs for chronic conditions like heart disease.

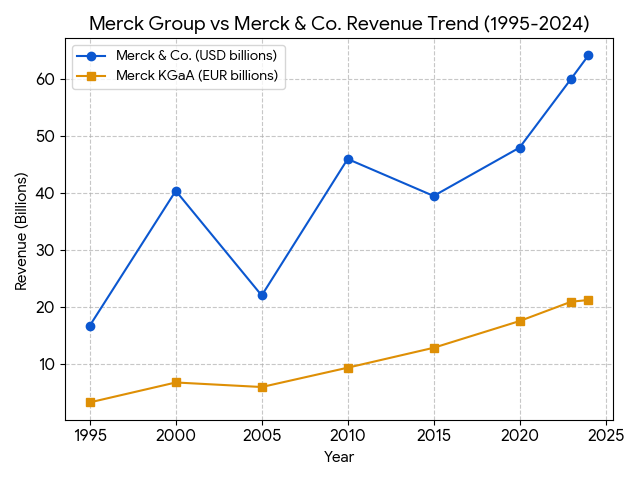

Revenue Level: * Germany: Reached billions of Euros; listed on the DAX in 1995.

- USA (MSD): Became one of the most profitable companies in the world, with revenue climbing into the tens of billions of USD.

Phase 4: Strategic Acquisitions and Specialization (2000–Present)

In the 21st century, both companies pivoted toward high-growth sectors like oncology and life science tools.

- Merck KGaA (The “Science & Technology” Pivot):

- They transformed into a leader in life sciences by acquiring Millipore (2010) and Sigma-Aldrich (2015).

- Acquired Versum Materials (2019) to become a dominant player in semiconductor materials (Electronics).

- Merck & Co. (The “Oncology & Biologics” Giant):

- 2009: Merged with Schering-Plough in a 41 billion dollar deal.

- Keytruda: Developed the anti-PD-1 therapy Keytruda, which became one of the best-selling cancer drugs in history.

- 2021: Spun off its legacy brands and women’s health business into a new company, Organon.

Core Products: * Germany: Millipore filters, Sigma-Aldrich reagents, and semiconductor precursor materials.

- USA (MSD): Keytruda (cancer immunotherapy) and Gardasil (HPV vaccine).

Core Strategy:

- Germany: Pivot to “Life Science Tools.” Through massive acquisitions (Millipore, Sigma-Aldrich), they became the primary supplier (the “pick-and-shovel” provider) for other biotech companies.

- USA (MSD): Focused on “Precision Oncology.” They spun off legacy products (Organon) to concentrate resources on biologics and immunology.

Revenue Level: * Germany: Approximately 21 billion EUR (2024); diversified revenue across Healthcare, Life Science, and Electronics.

- USA (MSD): Approximately 60 billion USD (2024), with Keytruda alone accounting for over 40% of total sales.

Keytruda (pembrolizumab) is the cornerstone of MSD’s portfolio. Its market dominance is driven by a massive clinical trial program (the KEYNOTE series) that has established it as a first-line therapy across dozens of cancer types.

1. Mechanism of Action (MoA)

Keytruda is a humanized monoclonal antibody that targets the PD-1 (Programmed Death receptor-1) pathway.

- Immune Evasion: Many cancer cells express ligands called PD-L1 and PD-L2. When these ligands bind to PD-1 receptors on T cells, they send an inhibitory signal that effectively “shuts off” the immune response, allowing the tumor to grow undetected.

- Checkpoint Blockade: Keytruda binds to the PD-1 receptor with high affinity, blocking its interaction with both PD-L1 and PD-L2. This “removes the brakes” from the immune system, reactivating cytotoxic T cells to recognize and kill tumor cells.

2. Clinical Efficacy Comparison (2025-2026 Data)

In 1L Non-Small Cell Lung Cancer (NSCLC), Keytruda remains the benchmark for survival, recently reinforced by large-scale real-world studies.

| Metric (1L NSCLC) | Keytruda (MSD) | Opdivo (BMS) | Tecentriq (Roche) |

| Survival Edge (2025 Study) | Benchmark | 17% lower risk of death vs Keytruda | 33% lower risk of death vs Keytruda |

| Median OS (mOS) | 26.3 Months | 17.1 Months | 20.2 Months |

| 5-Year Survival Rate | 31.9% | ~24.0% | ~22.0% |

| Key Strength | Broadest Label; Strongest Survival across PD-L1 levels | Strong IO+IO combinations (w/ Yervoy) | Leadership in SCLC and TNBC |

Note: Data based on KEYNOTE-024, CheckMate-227, and IMpower110 trials. A 2025 study of 4,600+ patients confirmed Keytruda’s survival superiority in older adults (66+) specifically.

3. Safety Profile: Adverse Events (AEs)

The safety of PD-1/PD-L1 inhibitors is generally characterized by immune-related Adverse Events (irAEs).

| Adverse Event | Keytruda (PD-1) | Opdivo (PD-1) | Tecentriq (PD-L1) |

| Grade 3-5 TRAEs | ~15-18% | ~14-16% | ~12-14% |

| Pneumonitis | 3.4% (Higher in post-radiation) | 2-4% | 1-3% |

| Hypothyroidism | 10-15% (Common) | 8-12% | 5-8% |

| Colitis/Diarrhea | 2-5% | 2-5% | 1-3% |

- Safety Observation: PD-L1 inhibitors (like Tecentriq) often show slightly lower rates of grade 3-5 toxicities because they do not block the PD-1/PD-L2 interaction, which helps maintain some peripheral immune tolerance.

4. Strategic Evolution: Subcutaneous (SC) vs. Intravenous (IV)

As of early 2026, the transition to subcutaneous formulations is a major competitive battleground.

- Injection Time: SC Keytruda takes approximately 2-3 minutes, compared to 30 minutes for IV infusion.

- Pharmacokinetics (Keynote-D77 Trial): * Trough Concentration ($C_{trough}$): SC showed a 67% increase compared to IV.

- Exposure (AUC): Confirmed non-inferiority ($p < 0.0001$).

- Efficacy: Objective Response Rate (ORR) was 45.4% (SC) vs. 42.1% (IV), proving the new delivery method does not compromise clinical outcomes.

Beyond subcutaneous (SC) reformulations, MSD’s pipeline is undergoing a massive transformation. As of early 2026, the strategy has shifted from finding a “better PD-1” to developing complex modalities—specifically Antibody-Drug Conjugates (ADCs) and Personalized Vaccines—that are much harder for biosimilar competitors to replicate.

Here are the most significant next-generation candidates currently in Phase 3 or pivotal stages:

1. Personalized Cancer Vaccines: mRNA-4157 (V940)

Developed in collaboration with Moderna, this is arguably the most “innovative” part of the pipeline.

- Mechanism: An individualized neoantigen therapy (INT) where mRNA codes for up to 34 unique mutations found in a patient’s specific tumor. It acts as a “GPS” for the immune system, while Keytruda removes the “brakes.”

- Latest Data (Jan 2026): Five-year follow-up from the Phase 2b KEYNOTE-942 trial in high-risk Melanoma showed a sustained 49% reduction in the risk of recurrence or death compared to Keytruda alone.

- 2026 Status: The Phase 3 INTerpath-001 trial is fully enrolled, with interim results expected later this year.

2. The “Precision Chemotherapy” Engine: Ifinatamab Deruxtecan (I-DXd)

MSD has pivoted heavily into ADCs through a multi-billion dollar deal with Daiichi Sankyo.

- Target: B7-H3, a protein highly expressed in Small Cell Lung Cancer (SCLC) and other neuroendocrine tumors but limited in healthy tissue.

- Clinical Performance: In the IDeate-Lung01 trial, it achieved a confirmed Objective Response Rate (ORR) of 48.2% in heavily pre-treated SCLC patients.

- 2026 Status: Currently in the Phase 3 IDeate-Lung02 trial. It received FDA Breakthrough Therapy Designation in late 2025, positioning it as a primary successor in the lung cancer market.

3. T-Cell Engagers: Gocatamig (MK-6070)

A specialized modality that physically links T cells to tumor cells.

- Mechanism: A tri-specific T-cell activating construct (TriTAC) targeting DLL3.

- Clinical Goal: Designed for “cold” tumors (like SCLC or Neuroendocrine Prostate Cancer) where Keytruda typically struggles.

- 2026 Status: Phase 1/2 trials have shown significant anti-tumor activity even in patients whose cancer has spread to the brain. It is being studied both as a monotherapy and in combination with I-DXd.

Pipeline Strategic Filter (Successors vs. Failures)

Not all candidates have survived the rigorous Phase 3 testing of 2024-2025. MSD has been aggressive in “cutting losers” to focus on high-probability winners:

| Candidate | Modality | Primary Target | 2026 Outlook |

| mRNA-4157 | mRNA Vaccine | Neoantigens | High Potential: Pivotal Phase 3 data in Melanoma/NSCLC pending. |

| I-DXd | ADC | B7-H3 | Strong Successor: Breakthrough status for SCLC. |

| MK-6070 | T-Cell Engager | DLL3 | Early Winner: Potential first-in-class for neuroendocrine tumors. |

| Favezelimab | mAb | LAG-3 | Discontinued: Development halted in Dec 2024 after failing Phase 3 in Colorectal Cancer. |

| Vibostolimab | mAb | TIGIT | Discontinued: Halted in late 2024 due to lack of efficacy in NSCLC trials. |

Summary for 2026

MSD is moving away from LAG-3 and TIGIT (traditional checkpoint inhibitors) and doubling down on ADCs and personalized mRNA technology. This shift creates a “dual-defense” against the 2028 patent cliff: one layer of protection via subcutaneous Keytruda and a second layer of growth via proprietary combination therapies that generic manufacturers cannot easily copy.

Comprehensive Analysis of Global HPV Vaccines (2026)

Beyond MSD’s Gardasil series, the global market has diversified significantly. As of 2026, the competition has evolved from a simple “Bivalent vs. Quadrivalent” debate into a multi-brand landscape involving various technological platforms.

I. Global HPV Vaccine Portfolio

| Vaccine Name | Manufacturer | Valency | Targets (HPV Types) | Platform (Expression System) |

| Gardasil 9 | MSD (Merck & Co.) | 9 | 6, 11, 16, 18, 31, 33, 45, 52, 58 | Saccharomyces cerevisiae (Yeast) |

| Cervarix | GSK | 2 | 16, 18 | Baculovirus (Insect Cells) |

| Cecolin | Innovax (Wantai) | 2 | 16, 18 | Escherichia coli (E. coli) |

| Cecolin 9 | Innovax (Wantai) | 9 | Same as Gardasil 9 | Escherichia coli (E. coli) |

| Walrinvax | Walvax (Zerun) | 2 | 16, 18 | Pichia pastoris (Yeast) |

| Cervavac | Serum Institute of India | 4 | 6, 11, 16, 18 | Saccharomyces cerevisiae (Yeast) |

II. Core Data Comparison: MSD vs. Emerging Competitors

1. Immunogenicity & Efficacy

- 9-Valent Competition (MSD vs. Wantai):

- Non-inferiority: Head-to-head trials in 2025–2026 confirmed that Cecolin 9 achieved a 100% seroconversion rate in females aged 18–26. The Geometric Mean Concentration (GMC) ratios compared to Gardasil 9 ranged from 0.78 to 1.91, meeting international non-inferiority standards.

- Long-term Protection: MSD maintains a “data moat” with over 10 years of longitudinal follow-up data. Chinese 9-valent brands (Wantai, Walvax) are currently in their 3–5 year follow-up phases.

- Bivalent Efficacy (GSK vs. Chinese Manufacturers):

- GSK Cervarix: Despite covering only two types, its proprietary AS04 adjuvant induces exceptionally high antibody titers and provides significant “cross-protection” against types 31, 33, and 45.

- Wantai Cecolin: While antibody titers are slightly lower than GSK’s, its efficacy in preventing CIN 2+ lesions related to types 16/18 remains near 100%.

2. Safety Profile

The safety profiles across all brands are remarkably similar, reflecting the maturity of HPV vaccine technology.

- Common Reactions: Localized injection site pain occurs in >80% of recipients, primarily due to the aluminum adjuvant triggering the immune response.

- Serious Adverse Events (SAEs): Across all approved vaccines, SAEs remain <0.1%, with no confirmed links to systemic autoimmune diseases.

3. Cost & Supply Chain

- Production Efficiency: Chinese manufacturers (e.g., Wantai) utilize E. coli-based systems, which offer significantly lower production costs and faster scalability compared to MSD’s yeast-based or GSK’s insect-cell systems.

- Pricing Impact: The entry of Cecolin 9 into the global market in 2025–2026 has begun to drive down procurement costs for international organizations like Gavi.

III. Key Trends in 2026

- Single-Dose Schedule: As of January 2026, the WHO-endorsed single-dose regimen has become the dominant schedule in 89 countries (including the U.S.). Data shows that one dose of Gardasil or Cervarix provides robust protection comparable to multi-dose regimens in long-term follow-ups.

- Gender-Neutral Programs: To combat the 2028 patent cliff, MSD is aggressively expanding Gardasil 9’s reach into the male market (preventing anal cancers and genital warts), which remains a key differentiator in high-income countries.

- Therapeutic Vaccines: Companies like Inovio (VGX-3100) are advancing DNA-based therapies aimed at treating existing HPV infections rather than just preventing them, with several candidates targeting FDA approval in late 2026.

Sources:

- Managed Healthcare Executive (Nov 2025): Survival Edge Study

- Journal of Thoracic Disease (Nov 2025): SC vs IV Comparison

- FDA/EMA Product Information (2025-2026 updates).

Back to Merck page