PetroChina’s history is deeply intertwined with the development of China’s energy industry. It has evolved from a government department into one of the largest integrated energy companies in the world. Its history can be categorized into four distinct stages:

Stage 1: The Ministry of Petroleum Industry (1950s–1980s)

During this period, the oil industry was managed under a planned economy with a “government-enterprise integration” model.

- 1955: The Ministry of Petroleum Industry was established to oversee national exploration.

- 1959: The discovery of the Daqing Oilfield marked a turning point, leading China toward energy self-sufficiency.

- The ministry acted as both the regulator and the operator of all oilfields.

Core Products: Crude oil, primarily from the Daqing oilfield (low-sulfur, high-wax content).

Core Strategy: Energy Self-Sufficiency. The goal was to maximize production volume to support national industrialization. Operations were funded by state budget allocations rather than market mechanisms.

Revenue Level: N/A (State-funded). In this era, oil was a strategic resource distributed by the state. Financial success was measured by production quotas (tonnage) rather than monetary profit or revenue.

Stage 2: Corporatization and CNPC Formation (1981–1998)

As China transitioned toward a market economy, the administrative structure was reformed to improve efficiency.

- 1988: The Ministry of Petroleum Industry was abolished and replaced by the China National Petroleum Corporation (CNPC).

- This shift moved the organization toward a corporate management style, though it still retained significant administrative functions.

Core Products: Crude oil, basic petrochemicals, and early-stage pipeline natural gas.

Core Strategy: Commercialization & Separation of Functions. Transitioning from a ministry to a corporation (CNPC). The strategy focused on improving extraction efficiency and starting small-scale international exploration.

Revenue Level: RMB 10s to 100s of Billions. As accounting systems became corporatized, revenue grew alongside China’s industrial demand, though it remained largely domestic and vertically fragmented.

Stage 3: Restructuring and International IPOs (1998–2000s)

This stage marked the birth of PetroChina as a modern, publicly traded corporation.

- 1998: A massive strategic reorganization of the Chinese oil and gas industry occurred. CNPC and Sinopec swapped assets to create two vertically integrated giants (upstream and downstream).

- 1999: PetroChina Company Limited (PetroChina) was officially incorporated as a subsidiary of CNPC, holding the majority of the parent company’s assets.

- 2000: PetroChina successfully launched its Initial Public Offering (IPO) on the New York Stock Exchange (as ADS) and the Hong Kong Stock Exchange.

Core Products: Refined products (Gasoline, Diesel), Jet Fuel, and Natural Gas.

Core Strategy: Integration & Low-Cost Growth. Achieving a “vertically integrated” model (Upstream + Downstream). The focus was on leveraging the domestic economic boom, expanding the gas station retail network, and utilizing capital from IPOs to modernize facilities.

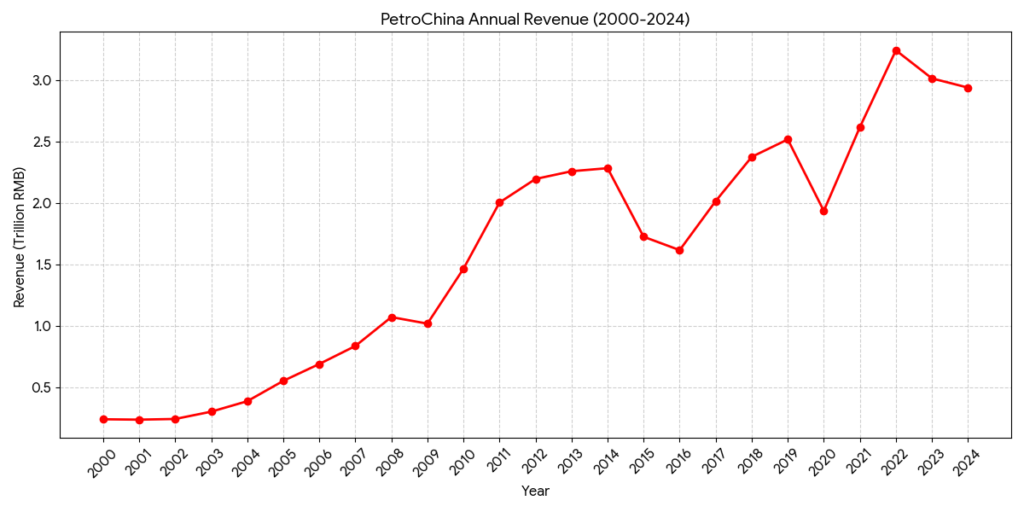

Revenue Level: RMB 200B to 800B. Revenue surged following the 2000 IPO. By the time it listed in Shanghai (2007), annual revenue had nearly quadrupled from its founding levels.

Stage 4: Global Expansion and Energy Transition (2007–Present)

The company expanded its global footprint while beginning to address climate and transition goals.

- 2007: PetroChina listed on the Shanghai Stock Exchange, briefly becoming the world’s first company with a market capitalization exceeding $1 trillion.

- Global Reach: The company aggressively invested in overseas projects in Central Asia, Africa, and South America to secure national energy supplies.

- Green Transition: In recent years, the company has pivoted toward a “Dual-Carbon” goal, investing in hydrogen, solar, and wind energy while aiming for near-zero emissions by 2050.

Core Products: Natural Gas (increasingly dominant), High-quality Chemicals, and New Energy (Hydrogen, Solar, Wind).

Core Strategy: “Stable Oil, Increasing Gas” & Green Transition. Strategic focus on overseas acquisitions (Central Asia, Middle East) to secure supply, while positioning Natural Gas as a “bridge fuel” toward a net-zero goal by 2050.

Revenue Level: RMB 2T to 3T+ (Trillion-level). Despite oil price volatility, revenue consistently stays in the multi-trillion range, making it one of the highest-revenue companies globally.

In 2026, the competitive landscape for PetroChina involves a two-tiered battle: maintaining dominance within the domestic “Big Three” oligopoly while competing with global supermajors amid a volatile energy transition.

1. Domestic Competition: The “Big Three” Dynamics

In China, the market is characterized by a stable but competitive division of labor between PetroChina, Sinopec, and CNOOC.

| Company | Core Strength | Competitive Weakness | 2026 Strategic Focus |

| PetroChina | Onshore Giant. Controls the majority of China’s onshore oil fields and gas pipelines. | Historical lag in downstream refining efficiency compared to Sinopec. | “Oil-to-Gas” Shift. Leveraging AI to optimize 2,500+ wells and accelerating shale gas extraction. |

| Sinopec | Refining & Retail King. Operates the world’s largest refining capacity and 30,000+ gas stations. | Low self-sufficiency in upstream resources; highly sensitive to global oil price spikes. | Hydrogen Leader. Transforming its retail network into “Integrated Energy Stations” (Oil + Hydrogen). |

| CNOOC | Offshore Expert. Industry-leading low lifting costs and deep-water expertise. | Minimal downstream presence; lacks a retail network to buffer upstream price drops. | Offshore Wind. Integrating traditional oil platforms with massive offshore wind farm projects. |

2. Global Competition: PetroChina vs. International Supermajors

On the global stage, PetroChina competes with the likes of ExxonMobil, Shell, and TotalEnergies for resources and capital.

- Scale vs. Valuation: While PetroChina’s revenue (approx. RMB 3T) rivals ExxonMobil, its valuation remains discounted. As of early 2026, its P/E ratio sits around 9.3x, significantly lower than the 12x-15x typical for U.S. giants, reflecting investor caution over state-owned governance.

- Cost of Production: PetroChina’s “cost per barrel” is generally higher than Middle Eastern producers but competitive with US shale. By 2026, the company has integrated machine learning to bring its break-even point below $45/barrel.

- The LNG Race: With massive new LNG capacities coming online from Qatar and the US in 2026, PetroChina faces intense price competition in the Asian gas market, despite its dominant domestic pipeline network.

3. Key Competitive Threats in 2026

Recent industry data points to three critical challenges:

- Global Supply Oversupply: The IEA predicts a surplus of 3.85 million barrels/day in 2026 due to record production in the Americas. This puts immense downward pressure on PetroChina’s upstream profit margins.

- Peak Oil Demand (Domestic): The rapid penetration of Electric Vehicles (EVs) in China is causing domestic fuel demand to peak earlier than expected. PetroChina must pivot its retail strategy from selling gasoline to providing “energy services.”

- ESG Transparency: International institutional investors are demanding more granular data on carbon intensity. While PetroChina has made strides in CCUS (Carbon Capture, Utilization, and Storage), it still trails European peers in ESG disclosure scores.

4. SWOT Summary for 2026

- Strengths: Monopoly over domestic gas infrastructure; strong state backing; massive onshore reserves.

- Weaknesses: Large workforce impacting operational agility; valuation “China discount”; high refining complexity.

- Opportunities: “Belt and Road” energy partnerships (Central Asia/Africa); technological breakthroughs in unconventional gas.

- Threats: Continued low oil price environment; aggressive EV adoption in China; geopolitical trade barriers.

PetroChina’s overseas competition in 2026 is defined by a shift from “volume-based expansion” to “efficiency-driven integration” and “green transition.” Unlike Western International Oil Companies (IOCs) that are under pressure to divest from fossil fuels, PetroChina leverages its state-backed status to secure strategic assets in emerging markets.

1. Overseas Revenue & Production (2024–2026)

As of early 2026, PetroChina’s overseas operations contribute roughly 10–15% of its total revenue, but they are critical for resource diversification.

- Production Volume: In 2024, overseas equity oil and gas production reached 112.9 million tons of oil equivalent, with a steady 2–3% annual growth targeted through 2026.

- Profitability: While global oil prices hovered around $70–$80/bbl in 2025, PetroChina’s overseas lifting costs remained competitive, particularly in Central Asia.

2. Competitive Advantages vs. IOCs (ExxonMobil, Shell, BP)

PetroChina utilizes a unique “NOC Model” that differs significantly from the “IOC Model.”

| Feature | PetroChina (NOC Model) | IOCs (Exxon, Shell, etc.) |

| Capital Access | State-backed loans with higher risk tolerance for strategic long-term projects. | Equity-funded; under strict pressure for immediate ROE and dividends. |

| Value Proposition | Package Deals. Bundles oil extraction with infrastructure (roads, hospitals, pipelines). | Technical Expertise. Focuses on high-margin, high-tech offshore or unconventional plays. |

| ESG Pressure | Primarily domestic policy-driven; slower to exit “brown” assets. | Intense pressure from Western institutional investors to divest from high-carbon assets. |

3. Regional Competitive Map (2026)

- Central Asia & Russia:

- Context: PetroChina’s “backyard.” Competition is low due to exclusive transnational pipeline agreements (e.g., Central Asia-China Gas Pipeline).

- Strategy: Deepening cooperation with Gazprom and KazMunayGas to secure land-based supply routes that bypass maritime chokepoints.

- Africa (The Middle East & Africa):

- Context: Direct competition with TotalEnergies and Eni.

- Strategy: While IOCs are exiting “difficult” onshore projects in Nigeria or Sudan due to security risks, PetroChina uses its superior risk tolerance and integrated construction capabilities to maintain and expand these assets.

- The Americas (South America & Deepwater):

- Context: Partnering with CNOOC and Petrobras in the Pre-salt fields.

- Strategy: Acting as a “non-operating partner” to learn deepwater drilling technology from Western peers while providing the necessary capital.

4. 2026 Strategic Challenges

- Local Content Requirements: Nations like Guyana and Brazil are enforcing stricter “Local Content” laws. PetroChina must move beyond “importing Chinese labor” to developing local supply chains, which increases operational costs.

- The “Divestment Gap”: As IOCs sell off mature assets to focus on renewables, PetroChina faces a dilemma: buy these “cheap” oil assets to boost production, or follow the global trend toward green energy to maintain international reputation.

- Geopolitical Sanctions: 2026 sees heightened scrutiny of energy trade. PetroChina must navigate complex compliance frameworks to avoid secondary sanctions on its overseas holdings.

Comparative Advantage Table

| Competitor Type | Key Threat to PetroChina | PetroChina’s Counter-Move |

| Regional NOCs (Aramco, Petronas) | Protection of home resources. | Joint Ventures (JVs) that include downstream refining in China. |

| Indian NOCs (ONGC) | Bidding wars for African/Central Asian assets. | Leveraging the “Belt and Road” infrastructure funding. |

| US Shale Producers | Low-cost export competition to Asia. | Strengthening long-term “Take-or-Pay” natural gas contracts. |

Sources:

- Mordor Intelligence – China Oil & Gas Market Analysis 2026

- IEA – Oil Market Report 2026 Outlook

- Simply Wall St – PetroChina (857) Competitor Analysis

Back to PetroChina page